-

Tax-Efficient Wealth Building: Strategies to Maximize Your Returns

Tips to Keep More of Your Hard-Earned Money Working for You

When it comes to preparing for a financially secure future, utilizing tax-efficient wealth building strategies can help you make the most of your assets. In fact, one often overlooked aspect of wealth building is the impact of taxes on investment returns. Implementing tax-efficient strategies can help you minimize tax liabilities and keep more of your hard-earned money working for you. In this article, we will explore various strategies that can optimize your investment returns and help you on your journey to tax-efficient wealth building.

Understand Tax-Advantaged Accounts

One of the foundational strategies for tax-efficient wealth building is leveraging tax-advantaged accounts. Familiarize yourself with options such as Individual Retirement Accounts (IRAs), 401(k) plans, Health Savings Accounts (HSAs), and 529 education savings plans. These accounts offer tax advantages, such as tax-deferred growth or tax-free withdrawals, allowing your investments to grow more efficiently.

Capitalize on Tax-Deferred Investments

Investing in tax-deferred vehicles can have a significant impact on your long-term wealth accumulation. Explore options like traditional IRAs, 401(k) plans, and deferred annuities. By deferring taxes on investment gains until withdrawal, you can potentially benefit from compounding growth and keep more of your returns working for you.

Utilize Tax-Efficient Asset Location

Strategic asset location involves placing different types of investments in the most appropriate accounts to optimize tax efficiency. For example, high-growth assets that generate significant capital gains may be best held in tax-advantaged accounts to defer taxes, while tax-efficient investments like index funds or tax-managed funds can be placed in taxable brokerage accounts. If you’re unsure about the tax treatments of different types of accounts, work with a financial advisor or tax professional to determine the most tax-efficient wealth-building strategies for your personal circumstances.

Harvest Tax Losses

Tax-loss harvesting involves strategically selling investments that have experienced losses to offset taxable gains. By realizing losses, you can reduce your tax liability while maintaining a similar investment position by reinvesting in similar assets. Careful consideration of tax rules and restrictions is crucial to ensure compliance and maximize the benefits of tax-efficient wealth building strategies like this one.

Long-Term Investing for Capital Gains

Holding investments for the long term can have substantial tax advantages. Capital gains from investments held for more than one year are subject to lower long-term capital gains tax rates. By adopting a long-term investment strategy, you can take advantage of these preferential tax rates and enhance after-tax returns.

Consider Tax-Efficient Investment Vehicles

Certain investment vehicles, such as exchange-traded funds (ETFs) or index funds, are designed to be tax-efficient. These funds aim to minimize taxable distributions by minimizing portfolio turnover or using in-kind transfers. Exploring these options can help you reduce taxable events and improve overall tax efficiency.

Charitable Giving

Charitable giving may strike you as an odd addition to a list of tax-efficient wealth building strategies, but these types of contributions offer potential tax benefits while supporting causes you care about. Consider donating appreciated securities directly to charitable organizations instead of cash. By doing so, you can potentially avoid capital gains taxes and still claim a deduction for the fair market value of the donated assets.

Related Article: Five Charitable Gifting Strategies That Come With Tax Advantages

Seek Professional Guidance

Navigating the complexities of tax-efficient wealth building can be challenging, and some of the above strategies may leave you feeling confused or overwhelmed if you try to go it alone. Consider working with a knowledgeable financial advisor or tax professional who can provide personalized guidance based on your unique financial situation. They can help you identify and implement the most effective tax strategies and ensure compliance with tax laws.

Are You Utilizing Tax-Efficient Wealth Building Strategies?

Building wealth requires a comprehensive approach that includes optimizing your investment returns while minimizing tax liabilities. By implementing tax-efficient wealth building strategies such as leveraging tax-advantaged accounts, capitalizing on tax-deferred investments, and utilizing strategic asset location, you can enhance your after-tax returns and accelerate your wealth-building journey. By making tax efficiency a priority, you can keep more of your wealth working for you and achieve greater long-term financial success.

If you’d like to discuss strategies for tax-efficient wealth building, contact Lane Hipple Wealth Management Group at our Moorestown, NJ office by calling 856-638-1855, emailing info@lanehipple.com, or to schedule a complimentary discovery call, use this link to find a convenient time.

Illuminated Advisors is the original creator of the content shared herein. I have been granted a license in perpetuity to publish this article on my website’s blog and share its contents on social media platforms. I have no right to distribute the articles, or any other content provided to me, or my Firm, by Illuminated Advisors in a printed or otherwise non-digital format. I am not permitted to use the content provided to me or my firm by Illuminated Advisors in videos, audio publications, or in books of any kind.

-

EQUITIES ADVANCE LAST WEEK AS THE FED RAISES RATES BY 25 BASIS POINTS

CORPORATE EARNINGS COME IN BETTER THAN EXPECTED

Summary

- The small-cap Russell 2000 (+1.1%) recorded another positive week, followed closely by the S&P 500 (+1.0%) and the DJIA (+0.7%)

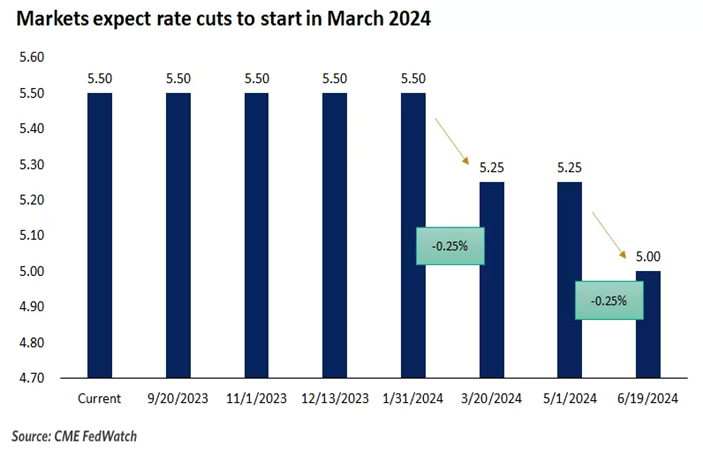

- There was a lot of economic news last week, but by far the biggest news was probably also the most expected, when the Fed voted on Wednesday to raise the target range for the fed funds rate by 25 basis points to 5.25-5.50%

- Surprisingly, Wall Street reacted well to the expected rate hike, on hopes that the Fed is done raising rates for the year, as the CME FedWatch Tool put the probability of a second rate hike any time later this year at less than 30%

- It was a busy earnings week, too, with Microsoft, Google (Alphabet) and Facebook (Meta) all moving decently

- Of the 11 S&P 500 sectors, 9 were positive as the Communication Services led the pack with a whopping 6.9% gain, whereas Utilities and Real Estate dropped by about 2% each

- The 10-year Treasury yield moved up 11 basis points and came to rest at 3.96%, a whisper away from that 4% threshold so important to Wall Street

Weekly Market Update – as of JULY 28, 2023

Close Week YTD DJIA 35,459 +0.7% +7.0% S&P 500 4,582 +1.0% +18.3% NASDAQ 14,317 +2.0% +36.8% Russell 2000 1,982 +1.1% +12.5% MSCI EAFE 2,196 +1.0% +13.0% Bond Index* 2,087.52 -0.35% +1.80% 10-Year Treasury 3.96% +0.11% +0.1% *Source: Bonds represented by the Bloomberg Barclays US Aggregate Bond TR USD.

This chart is for illustrative purposes only and does not represent the performance of any specific security. Past performance cannot guarantee future results

Stocks Advance as Fed Raises Rates

Stocks had a good week, as all four of the major U.S. equity indexes advanced on hopes that a soft landing engineered by the Federal Reserve was becoming real. Most encouraging for investors was the fact that the DJIA saw its 13th consecutive daily gain through Wednesday, marking its longest winning streak since 1987. Growth stocks far outpaced Value stocks, driven by NASDAQ’s 2% gain, which padded its 36%+ YTD gain.

The week’s biggest news was widely anticipated, as the Federal Reserve voted unanimously on Wednesday to raise the fed funds rate by 25 basis points, after pausing last month. Fed Chair Jerome Powell was non-committal about whether rates would be raised further, but he did acknowledge that inflation is far from its most-recent peak. The fed futures market is predicting that there will be about a 30% chance of another rate hike later this year.

There was a lot of economic data received last week and here are a few highlights:

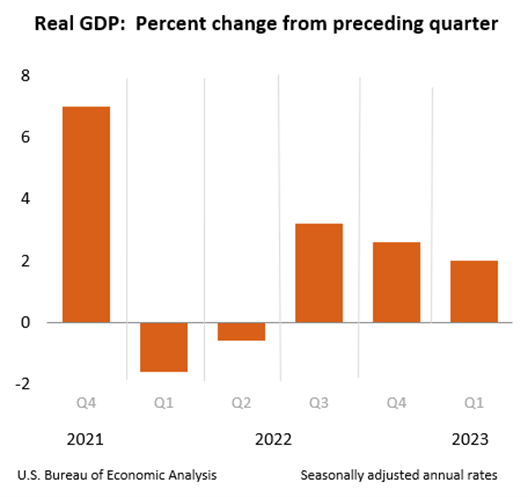

- Q1 GDP revised up significantly;

- New home sales jumped in May;

- New home sales prices declined in May;

- Durable goods orders advanced in May;

- Consumer confidence leapt in July;

- Personal income increased in May;

- Personal spending rose in May;

- Wages and salaries increased in May;

- Initial jobless claims dropped last week

GDP Revised Up Significantly

The third estimate for Q1 GDP saw a very large, upward revision to 2.0% from 1.3%, as consumer spending proved to be much more robust than anticipated.

Highlights

- Personal consumption expenditures growth was revised to 4.2% from 3.8%. That contributed 2.79 percentage points to Q1 GDP growth versus the second estimate of 2.52 percentage points.

- Gross private domestic investment declined 11.9%, versus the second estimate of -11.5%, after increasing 4.5% in Q4. This subtracted 2.22 percentage points from GDP growth versus 2.14 percentage points in the second estimate.

- Exports were up 7.8%, versus the second estimate of 5.2%, after declining 3.7% in Q4. Imports were up 2.0%, versus 4.0% in the second estimate, after declining 5.5% in Q4. Net exports contributed 0.58 percentage points to Q1 GDP growth versus the second estimate of 0.00 percentage points.

- Government spending increased 5.0%, versus the second estimate of 5.2%, after increasing 3.8% in Q4. This added 0.85 percentage points to Q1 GDP growth versus 0.89 percentage points in the second estimate.

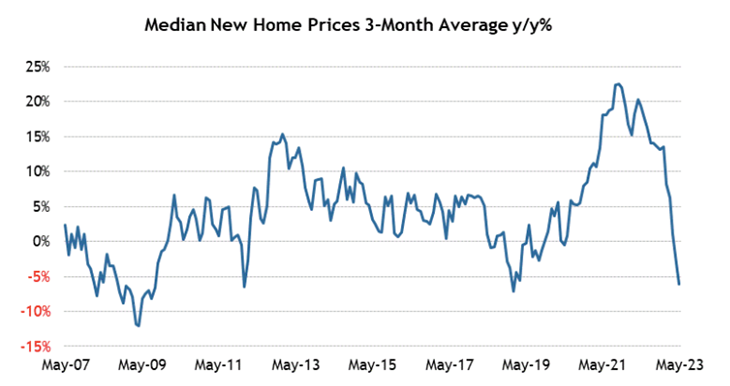

New Home Sales Jump in May But Sales Prices Decline

New home sales surged 12.2% month-over-month in May to a seasonally adjusted annual rate of 763,000 units. On a year-over-year basis, new home sales were up 20.0%, but the median sales price declined 7.6% year-over-year to $416,300 while the average sales price declined 6.6% to $487,300.

In addition:

- New home sales month-over-month/year-over-year by region:

- Northeast (+17.6%/+110.5%);

- Midwest (+4.1%/+40.0%);

- South (+11.3%/+22.0%);

- West (+17.4%/-0.6%).

- At the current sales pace, the supply of new homes for sale stood at 6.7 months, versus 7.6 months in April and 8.3 months in May 2022.

- The percentage of new homes sold for $399,999 or less accounted for 44% of new homes sold versus 49% in April and 39% one year ago.

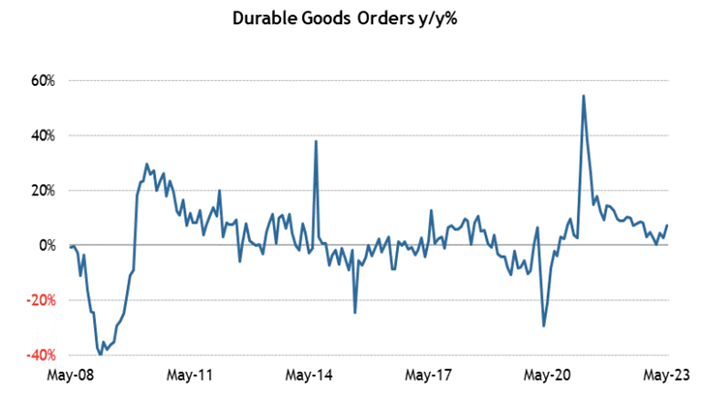

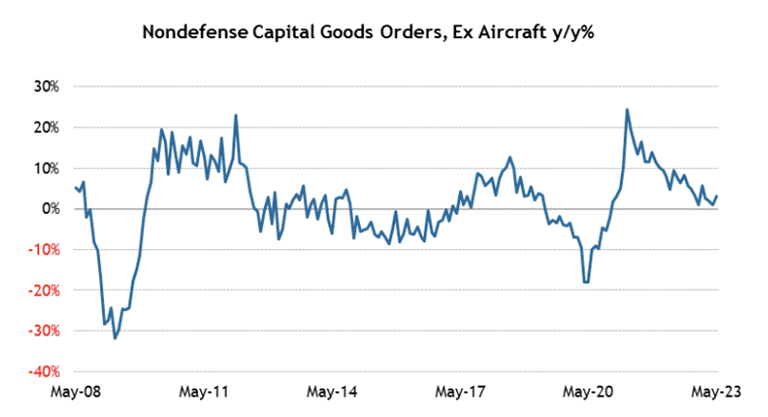

Durable Goods Orders Are UP

Total durable goods orders were up 1.7% month-over-month following an upwardly revised 1.2% increase (from 1.1%) in April. Excluding transportation, durable goods orders increased 0.6% month-over-month following a downwardly revised 0.6% decline (from -0.2%) in April.

Highlights

- New orders for machinery jumped 1.0% after increasing 0.3% in April.

- New orders for computers and electronic products increased 0.3% after declining 1.8% in April.

- New orders for fabricated metal products were flat after declining 0.2% in April.

- Transportation equipment orders jumped 3.9% after increasing 4.8% in April. New orders for motor vehicles and parts were up 2.2% after being flat in April. New orders for nondefense aircraft and parts rose 32.5% after slipping 2.0% in April.

- Shipments of nondefense capital goods excluding aircraft, which factors into GDP computations, increased 0.2% following a 0.4% increase in April.

Sources: conference-board.org; bea.gov; census.gov; msci.com; fidelity.com; nasdaq.com; wsj.com; morningstar.com

- The small-cap Russell 2000 (+1.1%) recorded another positive week, followed closely by the S&P 500 (+1.0%) and the DJIA (+0.7%)

-

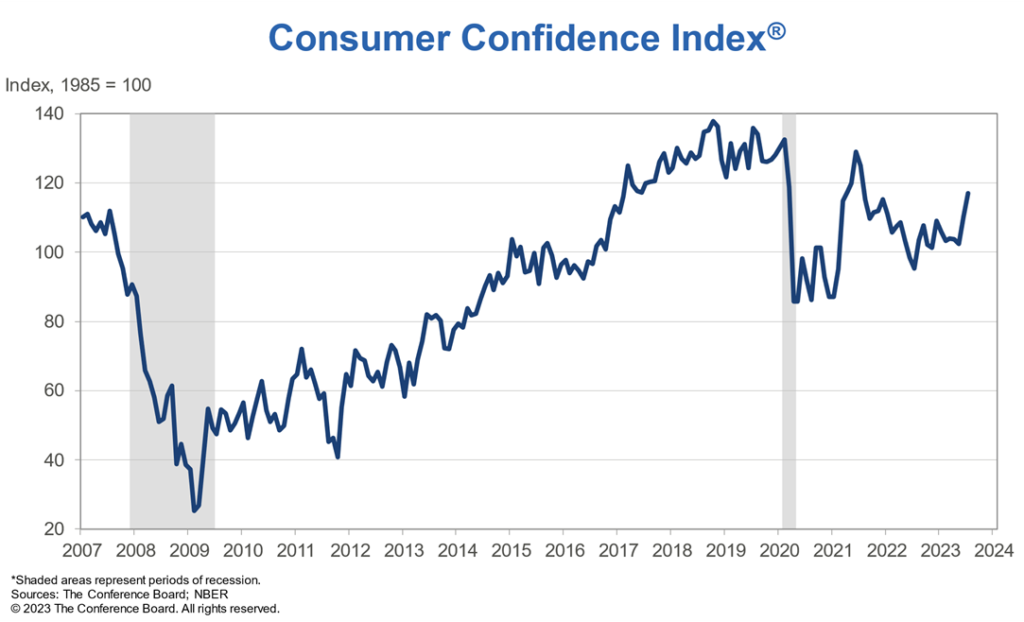

Consumer Confidence Up 2nd Month in A Row To Best Level Since July 2021

The Consumer Confidence Survey from the Conference Board “reflects prevailing business conditions and likely developments for the months ahead.”

This monthly Consumer Confidence report details consumer attitudes, buying intentions, vacation plans, and consumer expectations for inflation, stock prices, and interest rates. Data are available by age, income, 9 regions, and top 8 states.

On Tuesday, it was announced that the Conference Board Consumer Confidence Index rose again in July to 117.0 (1985=100), up from 110.1 in June.

Further:

- “The Present Situation Index – based on consumers’ assessment of current business and labor market conditions – improved to 160.0 (1985=100) from 155.3 last month.

- The Expectations Index – based on consumers’ short-term outlook for income, business, and labor market conditions – improved to 88.3 (1985=100) from 80.0 in June.

- Importantly, Expectations climbed well above 80 – the level that historically signals a recession within the next year. Despite rising interest rates, consumers are more upbeat, likely reflecting lower inflation and a tight labor market. Although consumers are less convinced of a recession ahead, we still anticipate one likely before year end.

Consumer confidence rose in July 2023 to its highest level since July 2021, reflecting pops in both current conditions and expectations. Headline confidence appears to have broken out of the sideways trend that prevailed for much of the last year. Greater confidence was evident across all age groups, and among both consumers earning incomes less than $50,000 and those making more than $100,000.”

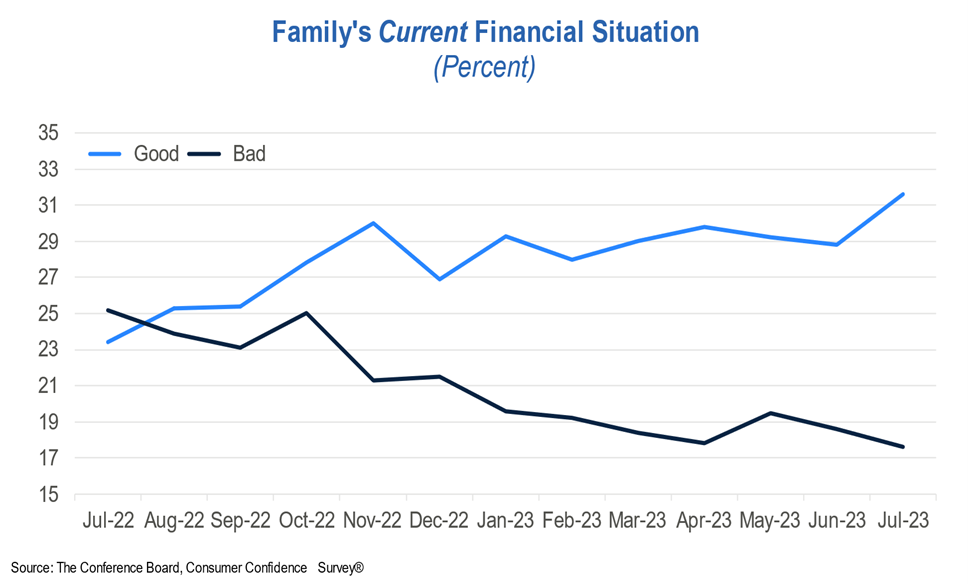

Family’s Current Financial Situation

Consumers’ assessment of their Family’s Current Financial Situation signals still-healthy family finances in July.

- 31.6% of consumers say their current family financial situation is “good,” up from 28.8% in June.

- 17.6% say their current family finances are “bad,” down from 18.6%.

Sources: conference-board.org

-

Bridging The Retirement Income Gap With FIAs

Authored By: Heather L. Schreiber, RICP® NSSA®

What do retirees fear most?

According to a GoBankingRates survey, 66% of Americans worry that they will run out of money during retirement. That’s ahead of the 50% who were concerned about a steep healthcare outlay¹.

How can seniors and their financial advocates address this worry? Many are choosing to do so with a fixed index annuity (FIA). LIMRA reports that FIA sales were $79.4 billion in 2022, up 25% from 2021, and 8% higher than the record set in 2019²’³. What’s so appealing about FIAs? Before the big reveal, let’s set the stage.

Shaky Stool

During the 20th century, a so-called 3-legged stool provided an underpinning for retirees’ finances. That is, cash flow could come from 3 sources: Social Security, pensions from former employers, and personal savings. However, employer pensions have become the exception rather than the rule for many retirees. Pensions are still common for long-term government workers but are relatively rare in the private sector.

Instead of pensions, private sector employers offer employees the opportunity to put wages into defined contribution plans such as 401(k)s. Generally, those dollars go into funds holding stocks and bonds. Recently, though, market

volatility has been in the headlines.Down Year

The Morningstar U.S. Market Index lost 19.4% in 2022, the biggest annual loss since 2008…when it lost a 38.4%. Bonds are supposed to offer stability when stocks sag, but the Morningstar U.S. Core Bond Index lost 12.9% in 2022, its biggest annual loss since inception of the index in 1993³.

To demonstrate the potential effect of such results on an approaching retirement, suppose a hypothetical Holly Smith retired in early 2022. At the start of that year, Holly had managed to accumulate $600,000 in retirement savings, evenly divided between stock funds and bond funds.Assume Holly’s investments matched the broad equity and fixed-income markets. At the start of 2023, her holdings would have been down to $241,800 in stocks and $261,300 in bonds—from $600,000 for retirement to just over $500,000. After such a loss, Holly would need almost a 20% gain just to get back to where she had been. Moreover, our Holly had retired in 2022, taking 4% of her savings ($24,000) to supplement Social Security last year. Now, Holly bears sequence-of-return risk, which impacts people whose retirement coincides with a bear market.

Holly’s choices might be taking that same $24,000 this year, from the $479,100 left in her portfolio. That’s a 5% withdrawal rate, which could lead to depletion while Holly is still alive. Or, Holly might stick to her 4% strategy, withdrawing only $19,164 (4% of $479,100) in 2023, which could mean cutting back on her lifestyle in retirement.

Financial markets have bounced back in the past, and that could be the case again, helping Holly’s portfolio last longer. Even with a rebound, retirees such as Holly face risks such as longevity that could eventually drain her portfolio, inflation that could strain her budget, and a need for costly long-term care. Threats to cut back on Social Security benefits add to Holly’s dilemma.

Mitigating Retirement Risks

Savvy planning can help take these key retirement risks off the table, or at least reduce them to the point where retirees are comfortable. Fixed Index Annuities (FIAs) can help mitigate these concerns to the extent that exceeds what other sources of retirement income can provide for retirees.

An FIA is funded either through a single lumpsum payment or a series of periodic contributions from a consumer to an insurance company. In exchange, the consumer receives a contract that may deliver tax-deferred buildup, principal protection in a down market, and growth potential. Increases to the annuity value, termed interest, are credited to the contract annually, tied to a market index such as the S&P 500. FIA dollars are not directly invested in the index components but are pegged to the results.

Generally, FIAs offer protection against market losses. In return, they usually provide lower upside potential than being invested directly in the market. With a crediting rate of 70% of the S&P 500, for example, a hypothetical 12-month index gain of 10% would generate a 7% crediting rate to the annuity value of an FIA with that provision. The tax-deferred nature of an FIA allows money to compound over time without having to pay ordinary income taxes on the growth until funds are withdrawn. Consumer have the choice of turning on a reliable income stream from an FIA for a period of time or for a lifetime to supplement other sources of income in retirement.

Related Article: Passing an Inheritance to Your Children: 8 Important Considerations

Bountiful Benefits

On the plus side, considering a fixed index annuity when building a retirement income strategy has several advantages which include:

Tax deferral. Any gains inside an FIA avoids immediate income tax, allowing the annuity owner to take advantage of pre-tax compound growth during the accumulation phase. FIA owners also benefit from flexibility in creating retirement income drawdown strategies by controlling when and how to take income from the annuity.

Asset allocation alternative. Conventional wisdom holds that a 60-40 split, stocks to bonds, combines the growth potential of equities with the stability of fixed income. However, both stocks and bonds suffered double-digit losses in 2022, as previously mentioned. Concerns of ongoing inflation may lead to hesitation regarding investing in bonds.

An income stream that retirees can’t outlive. Americans are living longer than ever. That generally equates to more time spent in retirement and pressure on retirement assets to last longer. Even with Social Security and perhaps other sources of dependable cash flow, there still may be a gap between actual income and desired annual outflow. An FIA can fill that gap, generating income that will last as long as the retiree (and perhaps a spouse) may live.

Principal protection against possible market losses. As explained above, sequence-of-returns risk occurs when financial markets drop early in retirement while a retiree is tapping his or her investment portfolio. That can cause lifelong savings to deplete more rapidly than would have been the case if those market corrections occur later in retirement. An FIA can protect retirement assets by offering a source of cash flow that is not exposed to this risk during a market downturn.

Income to allow deferral of Social Security benefits. Waiting to claim Social Security benefits, perhaps to as late as age 70, can increase lifelong payouts substantially and often increase payments to a surviving spouse. In order to finance such a delay while avoiding additional stress on other assets, an FIA can play a key role. A retiree might start tapping into an FIA at, say, age 62 to bridge income so that Social Security claiming occurs later. Seniors can make their accumulated retirement assets work smarter, not harder.

Support for a surviving spouse. When one spouse dies, the Social Security income benefit of the lower-earning spouse goes away, and the higher benefit is payable to the survivor. Loss of a spouse generally means a decline in income—going from two Social Security benefits to one survivor benefit—so depending on an FIA to replace lost income may be a strategy that can help the survivor maintain the same standard of living.

A hedge against unanticipated long-term care expenses in retirement. Standalone LTC insurance policies can be costly. Data from the American Association for Long-Term Care Insurance put the average premium for a 55-year-old couple on a $165,000 initial policy with a 3% annual growth in maximum coverage at approximately $5,025 per year³. That can be an unnecessary expense if the policy benefits are never used.

Nevertheless, LTC coverage may be necessary, because Medicare does not cover custodial LTC and the average cost nationwide for a private room in a nursing home is about $9,000 a month, according to Seniorliving.org⁴. Adding a long-term care rider to an FIA can provide an additional layer of protection, offsetting the potential expense of a need for LTC.

Spousal benefits. FIAs, when jointly owned, can create income streams over the course of two lives for a married couple. This can be extremely important because widow(er)s typically become single taxpayers, owing increased income tax. What’s more, a surviving spouse may not have much experience handling the couple’s finances. An FIA offering continued contract ownership to the survivor may provide tax deferral and market risk-free cash flow to an aging widow(er) in need of stable income.

Legacy planning: Non-qualified annuities, with properly named beneficiaries, may be utilized as an estate planning opportunity to permit non-spousal beneficiaries, such as the owner’s children, to stretch post-death withdrawals over decades, based upon their life expectancy. That’s because non-qualified annuities are not covered by SECURE Act’s 10-year rule.

Due Diligence

No financial product is perfect for every consumer in every situation, and that’s true for FIAs, too. These annuities may deliver exceptional results, but there are risks as well. For starters, any guarantees are backed by the issuer, so it’s necessary to evaluate the insurer’s financial strength; therefore, due diligence is vital. A knowledgeable financial professional can provide real value here.

In addition, FIAs may have costs, just as is the case with any financial product, such as an additional fee for an income rider. Again, a financial professional can help by determining the actual cost of buying a specific FIA to ensure that the product and associated costs meets the specific needs of the investor. The more that is known before buying an FIA, the greater the chance of enjoying the multiple benefits listed above.

Retirement Action Plan:

- Prepare early. Determine a realistic retirement timeline that considers income needs in retirement, source of retirement income, family history, and current investor health.

- Develop a plan that includes guaranteed income sources for predicable and necessary expenses. This plan should aim to fill any projected gaps.

- Recognize the various risks that come with any financial plan, including market risk, healthcare risk, inflation, loss of employment, or death of a loved one. Adjust the approach to minimize such concerns.

- Schedule a plan review at least annually with a knowledgeable financial professional and make needed changes.

- Consider including a fixed index annuity as part of a retirement income plan, to provide needed lifelong income without exposure to possible market weakness.

Sources

² www.morningstar.com/articles/1131213/just-how-bad-was-2022s-stock-and-bond-market-performance

³ www.aaltci.org/long-term-care-insurance/learning-center/ltcfacts-2022.php#2022costs

⁴ www.seniorliving.org/nursing-homes/costs/

Not affiliated with the Social Security Administration or any other government agency. This information is being provided only as a general source of information and is not intended to be the primary basis for financial decisions. It should not be construed as advice designed to meet the needs of an individual situation. Please seek the guidance of a professional regarding your specific financial needs. Consult with your tax advisor or attorney regarding specific tax or legal advice. ©2023 BILLC. All rights reserved. #23-0432-053024

-

Understanding the Fed’s Pause on Rate Hikes

Remain vigilant as we might see more rate hikes later this summer

The decision by the Federal Reserve to pause its upward trajectory of the federal funds rate – after 10 straight hikes over the past 14 months – has significant implications for investors. As the central bank of the United States, the Fed’s monetary policy decisions have a profound impact on financial markets and the investment landscape.

Let’s explore what this pause means for investors and explore potential strategies to navigate this new environment.

Understanding the Pause

To grasp the implications of the Fed’s pause, it is crucial to understand the underlying reasons for this shift in policy. The Federal Reserve’s primary mandate is to maintain price stability and support maximum employment. The decision to halt rate hikes suggests that the Fed believes inflationary pressures may be lessening or that the economy requires more time to fully recover. By pausing rate hikes, the central bank aims to provide ongoing support to economic growth.

Bond and Fixed-Income Investments

The Fed’s pause on rate hikes has immediate implications for bond and fixed-income investors. Typically, rising interest rates lead to declining bond prices. However, with the Fed indicating a pause in rate hikes, bond prices may stabilize or even experience modest gains. This is particularly relevant for long-term bondholders who were concerned about potential losses in a rising rate environment.

Nevertheless, investors should remain vigilant. While the pause in rate hikes may provide some relief, it is essential to monitor inflationary trends and the Federal Reserve’s future actions. Unexpected shifts in inflation expectations or the resumption of rate hikes could still impact fixed-income investments.

Equity Markets and Investment Strategies

The Fed’s pause on rate hikes can also have a significant impact on equity markets. Historically, low interest rates have been supportive of stock prices, as they reduce borrowing costs for businesses and increase the present value of future earnings. Investors should consider the potential for continued strength in equity markets as long as the pause in rate hikes persists.

However, it is crucial to exercise caution and avoid complacency. Market conditions can change rapidly, and investors should remain attentive to both global economic developments and the possibility of future rate hikes. Adopting a diversified investment strategy that balances exposure across sectors and geographies can help mitigate risks associated with potential market volatility.

Related Report: Charles Schwab’s Mid-Year Outlook

Sector Rotation and Asset Allocation

The pause in rate hikes offers an opportunity for investors to reassess their sector allocations and asset mix.

Certain sectors, such as utilities and real estate, tend to perform well in a low-interest-rate environment.

These sectors often exhibit stable cash flows and attractive dividend yields, making them appealing to income-focused investors.

Conversely, sectors like financials and banking may face challenges due to narrower interest rate spreads. Investors may consider rotating their investments into sectors that could benefit from the pause in rate hikes, while also maintaining a long-term perspective and keeping diversification in mind.

International Considerations

The Fed’s decision to pause rate hikes also has implications beyond the United States. Lower interest rates in the U.S. can lead to a weaker U.S. dollar, potentially benefiting international investments and exporters. Investors should consider the potential impact on currency valuations and diversify their portfolios by allocating a portion of their investments to international markets.

What Investors Should Do

The Federal Reserve’s pause on rate hikes represents a significant development for investors. The decision suggests that the central bank is carefully monitoring economic conditions and adjusting its policies accordingly. Bond and fixed-income investors may find some respite, while equity investors should remain attentive to potential shifts in market dynamics.

To navigate this evolving landscape, investors should adopt a diversified approach, reassess sector allocations, and consider the potential benefits of international investments.

Staying informed, monitoring economic indicators, and seeking professional advice can help investors make well-informed decisions in this environment of paused rate hikes. Even if it only lasts for a month.