-

Paying Off Your Mortgage vs. Investing More

What’s the Best Strategy for Your Financial Future?

Learn the Benefits and Drawbacks of Both Options

Are you wondering about the benefits and drawbacks of paying off your mortgage vs. investing? Paying off your mortgage early and investing more are both strategies that can help you achieve long-term financial stability, but it can be difficult to determine which goal to prioritize. In this article, we’ll explore the pros and cons of both strategies to help you determine which may be the best for your financial future.

Benefits of Paying Off Your Mortgage Early

First, let’s consider the benefits of paying off your mortgage early. It sounds ideal, right? You can save money in the long run and own your home outright more quickly than the terms of your loan determined. By making additional payments or accelerating your payment schedule, you can reduce the amount of interest you pay over the life of your loan, potentially saving tens of thousands of dollars. Additionally, paying off your mortgage early can provide a sense of financial security and peace of mind, as you will own your home outright and have no mortgage payment regardless of what the future may hold.

Drawbacks of Paying Off Your Mortgage Early

Of course, the question of paying off your mortgage vs. investing would be an easy decision if there were only clear benefits to one decision or the other. However, there are also some drawbacks to paying off your mortgage early. If you put all your extra money toward your mortgage, you may miss out on other opportunities to invest that money and earn higher returns. Additionally, if you focus too heavily on paying off your mortgage, you may not be able to take advantage of other financial opportunities, such as saving for retirement or building an emergency fund. So, before you opt for paying off your mortgage vs. investing more – or focusing on another important financial goal – consider the opportunity cost of putting all your financial eggs in one basket, so to speak.

Related Article: How Inflation Impacts Wealth Management and Investment Strategies

Benefits of Investing More

While there are clear benefits to paying off your mortgage vs. investing, don’t lose sight of the fact that investing more can be a powerful tool for building long-term wealth. By investing in stocks, mutual funds, or other assets, you have the potential to earn higher returns over time – potentially even outpacing the interest rate on your mortgage. Additionally, investing can provide diversification and help you build a well-rounded portfolio that can weather market fluctuations and economic downturns.

Drawbacks of Investing More

Investing, even in low-risk assets, does come with some risks. There is always a chance that you may lose money, particularly if you invest in riskier assets. Additionally, investing requires discipline and a long-term perspective. You must be prepared to weather market ups and downs, and not panic or make rash decisions when the market takes a downturn. If you already struggle with keeping your emotions in check with regard to your investments, it may not be best for you to significantly increase the dollar figure you’re investing.

Paying Off Your Mortgage vs. Investing More: What’s Right for You?

As with many financial decisions, what is best for your financial future truly comes down to your unique circumstances, goals, and priorities. If you value the security of owning your home outright and want to reduce your debt, paying off your mortgage early may be the best choice for you. On the other hand, if you’re willing to take on some risk and prioritize long-term wealth building, investing more may be the better choice.

At the end of the day, paying off your mortgage or investing more are both valid strategies for achieving long-term financial stability. By weighing the pros and cons of each approach and considering your individual circumstances and priorities, you can make an informed decision about which strategy is right for you.

If you’d like to discuss paying off your mortgage vs. investing more, contact Lane Hipple Wealth Management Group at our Moorestown, NJ office by calling 856-452-8026, emailing info@lanehipple.com, or to schedule a complimentary discovery call, use this link to find a convenient time.

Illuminated Advisors is the original creator of the content shared herein. I have been granted a license in perpetuity to publish this article on my website’s blog and share its contents on social media platforms. I have no right to distribute the articles, or any other content provided to me, or my Firm, by Illuminated Advisors in a printed or otherwise non-digital format. I am not permitted to use the content provided to me or my firm by Illuminated Advisors in videos, audio publications, or in books of any kind.

-

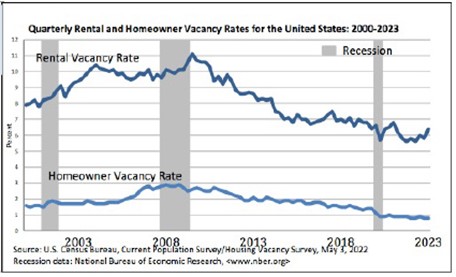

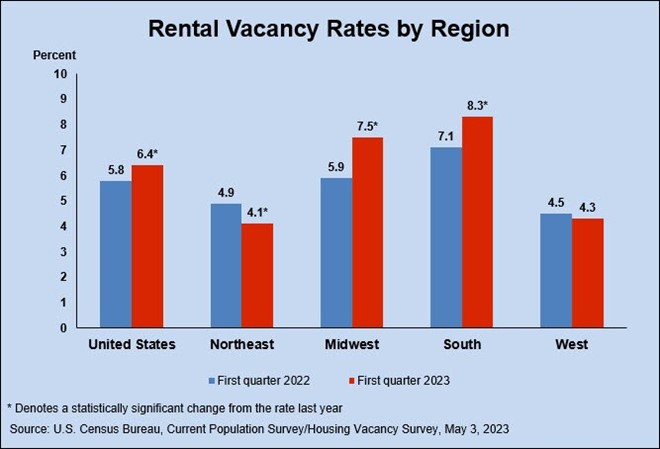

National Vacancy Rates Higher Versus This Time Last Quarter and Last Year

The U.S. Census Bureau announced the following residential vacancies and homeownership statistics for the first quarter 2023:

- National vacancy rates in the first quarter 2023 were 6.4% for rental housing and 0.8% for homeowner housing.

- The rental vacancy rate was higher than the rate in the first quarter 2022 (5.8%) and higher than the rate in the fourth quarter 2022 (5.8%).

- The homeowner vacancy rate of 0.8% was virtually the same as the rate in the first quarter 2022 (0.8%) and virtually the same as the rate in the fourth quarter 2022 (0.8%).

- The homeownership rate of 66.0% was not statistically different from the rate in the first quarter 2022 (65.4%) and not statistically different from the rate in the fourth quarter 2022 (65.9%).

- In the first quarter 2023, the median asking rent for vacant for rent units was $1,462.

- In the first quarter 2023, the median asking sales price for vacant for sale units was $319,000.

- Approximately 89.6% of the housing units in the United States in the first quarter 2023 were occupied and 10.4% were vacant.

- Owner-occupied housing units made up 59.1% of total housing units, while renter-occupied units made up 30.5% of the inventory in the first quarter 2023.

- Vacant year-round units comprised 7.9% of total housing units, while 2.5% were vacant for seasonal use.

- Approximately 2.1% of the total units were vacant for rent, 0.5% were vacant for sale only and 0.6% were rented or sold but not yet occupied.

- Vacant units that were held off market comprised 4.8% of the total housing stock – 1.5% were for occasional use, 0.8% were temporarily occupied by persons with usual residence elsewhere (URE) and 2.5% were vacant for a variety of other reasons.

Sources: census.gov

- National vacancy rates in the first quarter 2023 were 6.4% for rental housing and 0.8% for homeowner housing.

-

Are You Protecting Your Online Financial Information?

How to Keep Your Sensitive Information Safe from Cyber-Criminals

Do you manage some or all of your finances online? It’s a common – and convenient – practice today, but protecting your online financial information is of the utmost importance.

With the benefits of online banking and investing also comes the risk of cyber-attacks and identity theft. Hackers are becoming increasingly sophisticated in their methods, and it’s more important than ever to take steps to protect your online financial information.

In this article, we’ll explore some common threats to your online financial security and provide practical tips to help keep your sensitive information safe.

Common Cyber Attacks and Identity Theft Strategies

Knowledge is power when it comes to protecting your online financial information. There are numerous types of cyber-attacks and identity theft strategies to be aware of, so let’s review some of the most common scams:

Phishing

This is when cybercriminals use deceptive emails, phone calls, or text messages to trick people into providing their personal information or online financial information such as login credentials, Social Security numbers, or bank account details.

Malware Attacks

Malware refers to malicious software designed to damage or gain unauthorized access to a computer system. Cybercriminals use malware to steal personal information such as usernames and passwords, some of which may be used to access your bank accounts or other online financial information.

Ransomware Attacks

Ransomware is a specific type of malware that encrypts a victim’s files and demands payment in exchange for the decryption key. If the victim doesn’t pay, their files can be permanently lost or publicly released.

Social Engineering Attacks

This is when cybercriminals use human manipulation tactics to gain access to personal information. For example, they may impersonate a customer service representative and ask for login credentials.

Password Attacks

This includes brute force attacks where cyber criminals try numerous password combinations to gain access to a user’s account. It also includes password “spraying” where they use a list of commonly used passwords to gain access.

Account Takeover Attacks

This is when cybercriminals gain access to a user’s account by stealing their login credentials or using phishing attacks to trick them into revealing their information. If you become a victim and your information is available, cybercriminals may use it to access your online financial information, steal your identity, or perpetrate other criminal acts.

SIM Swapping

This is when a cybercriminal convinces a phone carrier to transfer a victim’s phone number to a new SIM card in their possession. They can then use this to gain access to accounts that use two-factor authentication via text message.

What You Can Do to Better Protect Your Online Financial Information

Threats like those described above are concerning, but it’s important to be aware. Of course, having awareness about threats to your online financial information is only half the battle. The other half is taking steps to keep your information safe. Here’s what you can do:

Use Strong Passwords

Your passwords should be complex, unique, and not used across multiple accounts. Avoid using obvious personal information such as your name, birth date, or address as part of your password. Consider using a password manager to generate and store strong passwords, making it easier to keep track of your various logins. Here’s a tutorial from Consumer Reports that may be helpful in getting started with a password manager.

Enable Two-Factor Authentication

Two-factor authentication adds an extra layer of security to your accounts by requiring you to enter a code sent to your phone or email in addition to your password. This ensures that even if someone gains access to your password, they still can’t log in without the second factor of authentication. Many financial institutions and other online services offer this added security feature, so be sure to enable it whenever possible.

New Article: Social Security for Divorced Individuals

Be Wary of Phishing Scams

Phishing scams, as described above, are fraudulent attempts to obtain your personal information, such as your login credentials, credit card numbers, and other sensitive online financial information. These scams often come in the form of unsolicited emails, texts, or phone calls that appear to be from a legitimate source, such as your bank or an online retailer. Be cautious when entering personal information on unfamiliar websites and avoid clicking on links or downloading attachments from unsolicited emails.

Keep Your Software Up to Date

Software updates often include security patches that address vulnerabilities and protect against the latest threats. Make sure to install updates for your operating system, web browser, and other software as soon as they become available. This will help keep your devices and accounts secure from potential cyberattacks.

Monitor Your Accounts Regularly

Most of us don’t have time to monitor all our online financial information daily, or even weekly. However, it’s important to check your bank and credit card statements regularly – at least monthly – for any suspicious activity and report any unauthorized transactions immediately. It’s also a good idea to review your credit reports periodically to ensure that no one has opened new accounts in your name. The sooner you catch any fraudulent activity, the easier it will be to resolve the issue and prevent further damage.

Are You Protecting Your Online Financial Information?

It’s easy to assume that all of your online financial accounts have built-in protections from common scams – and most do. However, it’s critical to be sure you’re activating optional steps, like two-factor authentication so that your accounts are as protected as possible. By following the above tips, you can help protect your online financial information and reduce the risk of falling victim to fraud or identity theft. Remember to stay vigilant and be proactive in keeping your personal and financial data secure.

If you’d like to discuss more about safe ways to use online financial accounts, contact Lane Hipple Wealth Management Group at our Moorestown, NJ office by calling 856-249-4342, emailing info@lanehipple.com, or to schedule a complimentary discovery call, use this link to find a convenient time.

Illuminated Advisors is the original creator of the content shared herein. I have been granted a license in perpetuity to publish this article on my website’s blog and share its contents on social media platforms. I have no right to distribute the articles, or any other content provided to me, or my Firm, by Illuminated Advisors in a printed or otherwise non-digital format. I am not permitted to use the content provided to me or my firm by Illuminated Advisors in videos, audio publications, or in books of any kind.

-

Social Security for Divorced Individuals

Written by Elaine Floyd, CFP®

If there is one key differentiator between baby boomers and their parents, it is the higher incidence of divorce.

Americans over 50 are twice as likely to be divorced compared to the same age group 20 years ago.

If you have been divorced in the past and are currently unmarried, you may be able to qualify for Social Security benefits based on your ex-spouse’s work record. In order to qualify for a divorced-spouse benefit you must:

- Be age 62 or older

- Be finally divorced from the worker on whose record benefits are being claimed

- Have been married for over 10 years

- Be currently unmarried

Your ex-spouse must be at least age 62. If the divorce occurred more than two years prior, your ex-spouse does not need to have filed for his or her own retirement benefit.

Example: Michael and Maria were married over 10 years. They have been divorced over two years. Both are age 62. Maria has not remarried. Maria is eligible for a divorced-spouse benefit based on Michael’s work record, regardless of whether or not Michael has filed for his benefit.

If you claim your divorced-spouse benefit at full retirement age or later (66 for those born before 1954, increasing gradually to 67), your benefit will be 50% of your ex-spouse’s primary insurance amount (PIA). The primary insurance amount is the amount your ex-spouse will receive if he claims his benefit at full retirement age.

Example: Jim and Judy are divorced. Jim’s PIA is $2,400. Judy files for her divorced-spouse benefit at age 66. She will receive 50% of Jim’s PIA, or $1,200, as her divorced-spouse benefit.

What if you also qualify for Social Security on your own work record?

If you also worked and qualify for a Social Security benefit based on your own work record, you may be able to coordinate your divorced-spouse benefit with your own retirement benefit in order to maximize each type of benefit. But you must get the timing right.

Don’t file at 62. If you file for Social Security at age 62, you may not be able to receive a divorced-spouse benefit. That’s because you will be required to take your own reduced benefit first. If your PIA is more than one-half of your ex-spouse’s PIA, you will not ever be able to receive a divorced-spouse benefit.

Example: Sam and Sue are divorced after being married more than 10 years. Sam’s PIA is $2,400. Sue’s PIA is $2,200. If Sue files for Social Security at 62, she will be forced to receive her own reduced benefit of $1,650 (75% of $2,200). Since her PIA is more than one-half of Sam’s PIA, she will not ever be able to receive a divorced spouse benefit. The $1,650 will be her permanent benefit except for annual cost-of-living adjustments.

File a restricted application at FRA. To receive a divorced-spouse benefit while your own benefit builds delayed credits – an ideal strategy for divorced people – you can file a restricted application for your divorced spouse benefit at full retirement age and switch to your own maximum retirement benefit at age 70.

Example: If Sue, from the above example, waits until age 66 to file a restricted application for her divorced-spouse benefit, she can receive 50% of Sam’s PIA, or $1,200 from age 66 to 70. At age 70, she can switch to her own maximum retirement benefit of $2,904 ($2,200 x 1.32). This is Sue’s optimal Social Security claiming strategy, allowing her to maximize both benefits and giving her the highest lifetime benefits.

Note: The Budget Act of 2015 is phasing out the ability to file a restricted application. You must have attained age 62 by January 1, 2016 to file a restricted application for spousal benefits. If you are not able to file a restricted application, you may still be eligible to receive a divorced-spouse benefit, but only if it is higher than your own benefit.

Mechanics of filing

To file for a divorced-spouse benefit, you need not be in contact with your ex-spouse. Your ex-spouse’s current marital status is not relevant. In fact, if your ex-spouse has remarried, the current spouse and any other ex-spouses can also receive benefits without affecting your divorced-spouse benefit. Or, if your ex-spouse has not remarried, he (or she) can claim a divorced-spouse benefit off your record. Unlike with spousal benefits, two divorced spouses can each claim a spousal benefit off the other’s record at the same time.

If you are not in contact with your ex-spouse, it may be difficult to estimate the amount of your divorced-spouse benefit. Due to privacy issues, the Social Security Administration will not give out this information until you are ready to apply for the benefit.

You can generally ballpark your ex-spouse’s PIA at somewhere between $2,000 and $2,600. Your divorced spouse benefit will be 50% of that amount if you file for it at your full retirement age.

To file for your divorced-spouse benefit, you will need to make an appointment with your local Social Security office and show a certified copy of the divorce decree. It is helpful to have your ex-spouse’s Social Security number (you can get it off an old tax return), but not essential.

If you do not have your divorce papers you can order a certified copy through VitalChek, www.vitalchek. com. If your marriage lasted right around ten years and you’re not sure if you meet the ten-year requirement, check the date on the divorce decree; some people are surprised to learn that the actual date of dissolution is later than they had thought.

Ex-spouse deceased?

If your ex-spouse has died, and if you were married at least ten years, you may qualify for a divorced-spouse survivor benefit. If you apply for it at your full retirement age or later, the benefit amount will be 100% of his PIA, or, if he had already started benefits, the amount your ex-spouse was receiving at the time of death.

As with divorced-spouse benefits, you can sequence the timing of the survivor benefit and your own retirement benefit to maximize each benefit. For example, you could apply for a reduced divorced-spouse survivor benefit as early as age 60 (50 if disabled) and then switch to your own maximum retirement benefit at age 70. Or you might do it the other way: start your own reduced retirement benefit at age 62 and switch to your maximum survivor benefit at full retirement age. Your financial advisor can help you determine the optimal strategy.

More than one ex-spouse?

If you were married two (or three) times and each marriage lasted more than ten years, you can choose which ex-spouse’s record to draw from. In fact, you can sequence these benefits for maximum advantage, essentially taking advantage of several benefits, just not at the same time. It can get complicated. Your advisor and SSA can help you sort it all out.

Think twice before remarrying

Keep in mind that divorced-spouse benefits must stop upon remarriage. You cannot receive a divorced spouse benefit if you are married (one exception: the divorced-spouse benefit may continue if the person you marry is receiving survivor benefits at the time of the remarriage). But also consider the potential spousal benefit from your new spouse. If you are receiving a divorced-spouse benefit at the time of your remarriage, that benefit would stop but you may immediately start receiving a spousal benefit based on your new spouse’s earnings record without waiting the usual one year for spousal benefits.

So here you might want to compare the two benefits and either remarry or remain single depending on which benefit is higher.

If your ex-spouse is deceased, divorced-spouse survivor benefits would not be available to you if you remarry before age 60. Or, to put it another way, if you remarry after age 60, you may still receive a divorced-spouse survivor benefit based on the earnings record of your ex-spouse who has died.

The bottom line: if you are eligible for divorced-spouse benefits or divorced-spouse survivor benefits and are thinking of remarrying, consider delaying the marriage. If your ex is still alive (and has a higher PIA than your new potential spouse), remarriage at age 70 will allow you to receive full divorced-spouse benefits from age 66 to 70, when you would switch to your own maximum retirement benefit. If your ex is deceased, you can remarry anytime after age 60 without jeopardizing your divorced-spouse survivor benefit.

Talk to the Social Security Administration and to your financial advisor about the best claiming strategy for you based on your personal circumstances.

Elaine Floyd, CFP®, is Director of Retirement and Life Planning for Horsesmouth, LLC, where she focuses on helping people understand the practical and technical aspects of retirement income planning.

Copyright © 2023 by Horsesmouth, LLC. All rights reserved. IMPORTANT NOTICE This reprint is provided exclusively for use by the licensee, including for client education, and is subject to applicable copyright laws. Unauthorized use, reproduction or distribution of this material is a violation of federal law and punishable by civil and criminal penalty. This material is furnished “as is” without warranty of any kind. Its accuracy and completeness is not guaranteed and all warranties expressed or implied are hereby excluded.

-

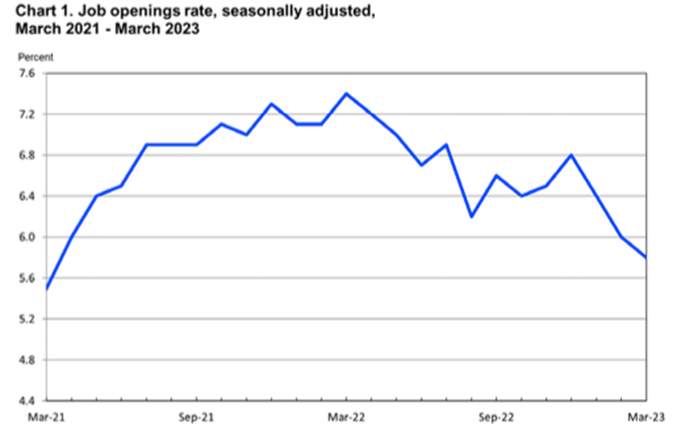

Number of Job Openings Drops for 3rd Month to Lowest Level in 2 Years

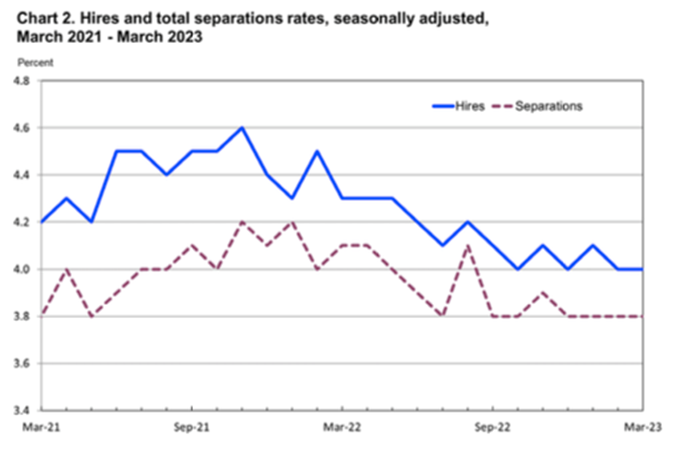

The number of job openings decreased to 9.6 million on the last business day of March, according to the U.S. Bureau of Labor Statistics. Over the month, the number of hires and total separations were little changed at 6.1 million and 5.9 million, respectively. Within separations, quits (3.9 million) changed little, while layoffs and discharges (1.8 million) increased. This release includes estimates of the number and rate of job openings, hires, and separations for the total nonfarm sector, by industry, and by establishment size class.

Job Openings

On the last business day of March, the number of job openings decreased to 9.6 million (-384,000) and was 1.6 million lower than in December. The job openings rate was 5.8% in March and was down by 1.0 percentage point since December. In March, job openings decreased in transportation, warehousing, and utilities (-144,000) but increased in educational services (+28,000).

Hires

In March, the number of hires was little changed at 6.1 million, and the rate held at 4.0%. Hires decreased in real estate and rental and leasing (-29,000).

Separations

The number of total separations changed little at 5.9 million in March, and the rate was 3.8% for the fourth month in a row. Over the month, the number of total separations decreased in accommodation and food services (-107,000) but increased in construction (+104,000).

In March, the number and rate of quits changed little at 3.9 million and 2.5%, respectively. The number of quits decreased in accommodation and food services (-178,000). In March, the number and rate of layoffs and discharges increased to 1.8 million (+248,000) and 1.2%, respectively. Layoffs and discharges increased in construction (+112,000), accommodation and food services (+63,000), and health care and social assistance (+42,000).

The number of other separations was little changed in March at 276,000. Other separations decreased in finance and insurance (-31,000) and in real estate and rental and leasing (-7,000).

Sources: bls.gov