-

It’s Back to School Time: Does Your Retirement Savings Plan Earn a Passing Grade?

Here’s How to Give Your Financial Education a Boost

They don’t often teach how to create a retirement savings plan in school, but it’s time to put your thinking cap on and ask yourself a question: what grade would your retirement savings plan earn if it was put to the test today?

It’s tough to know exactly how much you should save, what strategies might work for you, and exactly how to get to where you want to be. Just like in the classroom, though, the best way to get a passing grade for your retirement savings plan is to educate yourself and put in the effort.

If you aren’t sure where you stand – or you know that your plan could be strengthened – the following advice can help you cram for your retirement savings plan.

First, if you don’t feel like you’ve earned an A+ on the retirement progress you’ve made to-date, know that you’re not alone. The Road to Retirement Survey from TD Ameritrade found that most Americans feel like they’re doing poorly saving for retirement. Of surveyed adults ages 40 to 79, the majority gave themselves a grade of C or lower. This result seems fair when you look at the data, too. Nearly two thirds of 40-year-olds have less than $100K saved for retirement, and one in five of those in their 70s have less than $50K saved.

If you’re in this boat, these steps will help:

1. Keep building your nest egg

There are many reasons people can’t seem to attain the savings they need. Yet there are as many reasons you should save for retirement as there are excuses not to. Even if you’re only able to save a small amount at present, stay the course. It all makes a difference down the road.

If you’re under 40 and have saved even a small amount, you’ve got several decades ahead of you to make up for any lost time. If you start putting away $500 a month in an IRA or 401(k), you could retire in 25 years with an additional $380,000, assuming a conservative annual average of 7% market returns during that time.

If you’re closer to 60 than to 40, though, you have less time to get your retirement savings plan right. Putting money into savings now will mean you struggle less in the future. Consider some big-time ways to sock away more money—maybe a second job, moving to a smaller home with a smaller mortgage, or other ways to build up your savings.

Say you’re around 57 years old and want to retire in a decade. If you save $500 a month for the next 10 years, you’ll only be able to save $83,000, assuming the same conservative 7% rate of return mentioned above. If you double that and put away $1,000 a month instead, you’ll double your savings amount. While $166,000 may seem like a lot of cash, it’s hard to stretch that through your retirement years. Instead, consider readjusting your lifestyle and maxing out your 401(k).

2. Increase your Social Security benefits

Social Security benefits can help anyone approaching retirement have peace of mind. Avoid making the mistake of depending too much on them, though. As the system works now, benefits are projected to replace around 40% of the average American’s preretirement income, but most people need around 80% of their former earnings to live at the comfort level they’re accustomed to.

Still, there are significant benefits to Social Security. It’s a government-backed, 8% guaranteed investment. Navigating the system can be complicated, but there are ways you can plan to get the most out of your retirement options, especially these days a people live much longer than they used to.

These tips can help you increase your Social Security income:

- Earn as much as you can right up until full retirement age (usually 66 years old), or even beyond

- Work at least 35 years or more

- Wait as long as possible to claim (If you wait until age 70, you can boost your benefit by 8% a year)

- Pay attention to taxes—50% to 85% of your benefits could be subject to federal taxes if you reach a certain income threshold

These strategies are helpful, but remember that even if you maximize your Social Security benefit in these ways, you’ll likely still have to make up the difference with personal savings. So, preparation is critical.

Related Article: Retirement Planning: How to Live Like It’s Summer Vacation Forever

3. Boost your retirement readiness grade

If you have concerns about your retirement savings plan, the good news is that there are different strategies for different stages in life. No matter where you are, there are ways to plan and prepare for where you want to be.

When it comes to retirement, having your finances in order is about more than just money. It’s a direct indication of how much you’ll be able to savor that chapter of your life.

It’s important to consider how ready you are. Do you make the grade, or are you like one of the many Americans who barely pass the retirement readiness test? Readiness requires discipline, clearly defined goals, and actionable plans. This requires quite a bit of hard work and preparation, but the result is enjoying and maintaining the same standard of living you’ve experienced while in the working world.

Get A+ Strategies for Your Retirement Savings Plan

If you think you would benefit from expert help with your retirement readiness plan, contact Lane Hipple Wealth Management Group at our Moorestown, NJ office by calling 856-638-1855, emailing info@lanehipple.com, or to schedule a complimentary discovery call, use this link to find a convenient time.

Illuminated Advisors is the original creator of the content shared herein. We have been granted a license in perpetuity to publish this article on our website’s blog and share its contents on social media platforms. We have no right to distribute the articles, or any other content provided to our Firm, by Illuminated Advisors in a printed or otherwise non-digital format. We are not permitted to use the content provided to us or my firm by Illuminated Advisors in videos, audio publications, or in books of any kind.

-

5 Things You Need To Know To Ride Out A Volatile Stock Market

This article, written by Franklin Distributors, LLC, provides great insight on how to approach today’s investment environment.

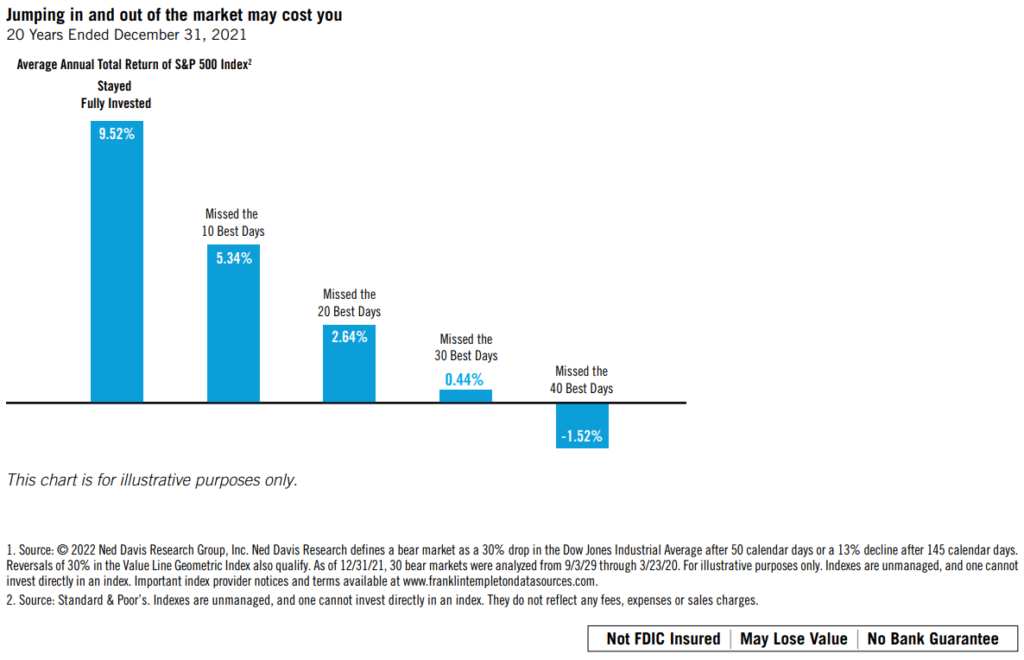

1. Watching from the sidelines may cost you

When markets become volatile, a lot of people try to guess when stocks will bottom out. In the meantime, they often park their investments in cash. But just as many investors are slow to recognize a retreating stock market, many also fail to see an upward trend in the market until after they have missed opportunities for gains. Missing out on these opportunities can take a big bite out of your returns. Consider that on average, for the 12 months following the end of a bear market, a fully invested stock portfolio had an average total return of 38.3%. However, if an investor missed the first six months of the recovery by holding cash, their return would have been only 8.0%¹. The chart below is a hypothetical illustration showing the risk of trying to time the market. By missing just a few of the stock market’s best single-day advances, you could put a real crimp in your potential returns.

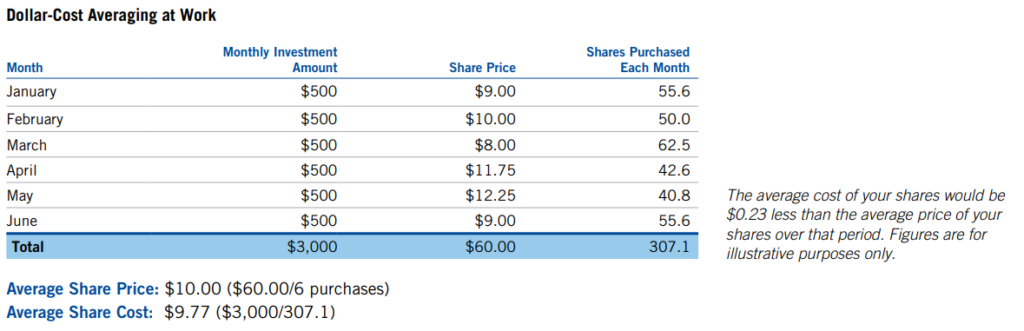

2. Dollar-cost averaging makes it easier to cope with volatility

Most people are quick to agree that volatile markets may present buying opportunities for investors with a long-term horizon. But mustering the discipline to make purchases during a volatile market can be difficult. You can’t help wondering, “Is this really the right time to buy?”

Dollar-cost averaging can help reduce anxiety about the investment process. Simply put, dollar-cost averaging is committing a fixed amount of money at regular intervals to an investment. You buy more shares when prices are low and fewer shares when prices are high. And over time, your average cost per share may be less than the average price per share. Dollar-cost averaging involves a continuous, disciplined investment in fund shares, regardless of fluctuating price levels. Investors should consider their financial ability to continue purchases through periods of low price levels or changing economic conditions. Such a plan does not guarantee a profit or eliminate risk, nor does it protect against loss in a declining market.

3. Now may be a great time for a portfolio checkup

Is your portfolio as diversified as you think it is? Meet with your financial professional to find out. Your portfolio’s weightings in different asset classes may shift over time as one investment performs better or worse than another. Together with your financial professional, you can re-examine your portfolio to see if you are properly diversified. You can also determine whether your current portfolio mix is still a suitable match with your goals and risk tolerance.

4. Tune out the noise and gain a longer-term perspective

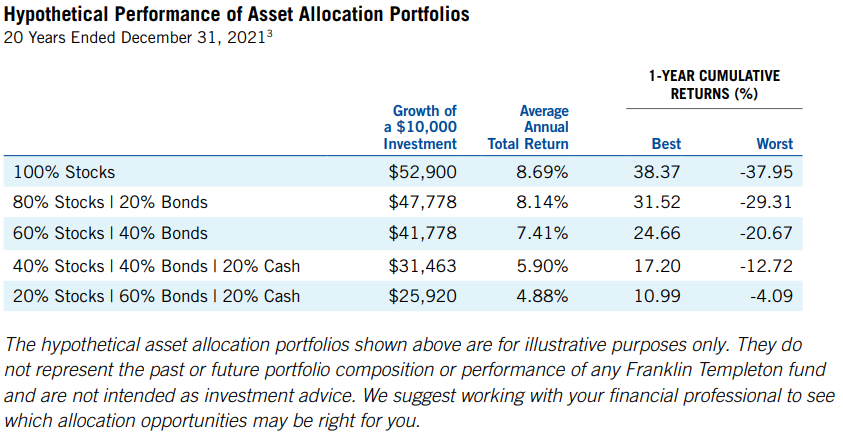

Numerous television stations, websites and social media channels are dedicated to reporting investment news 24 hours a day, seven days a week. What’s more, there are almost too many financial publications to count. While the media provides a valuable service, they typically offer a very short-term outlook. To put your own investment plan in a longer-term perspective and bolster your confidence, you may want to look at how different types of portfolios have performed over time.

- Source: © 2022 Morningstar, Inc., 12/31/21. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance does not guarantee future results. Stock investments are represented by equal investments in the S&P 500 Index, Russell 2000® Index, and MSCI EAFE Index, representing large U.S. stocks, small U.S. stocks, and foreign stocks, respectively. Bonds are represented by the Bloomberg Barclays U.S. Aggregate Index. Cash equivalents are represented by the FTSE 3-Month U.S. Treasury Bill Index. Portfolios are rebalanced annually. Indexes are unmanaged, and one cannot invest directly in an index. They do not reflect any fees, expenses or sales charges.

5. Believe your beliefs and doubt your doubts

There are no real secrets to managing volatility. Most investors already know that the best way to navigate a choppy market is to have a good long-term plan and a well-diversified portfolio. But sticking to these fundamental beliefs is sometimes easier said than done. When put to the test, you sometimes begin doubting your beliefs and believing your

doubts, which can lead to short-term moves that divert you from your long-term goals.To keep a balance perspective, we recommend that you contact your financial professional before making any changes to your portfolio.

-

Focus on Your Financial Freedom this Independence Day

Five Steps to Declare Your Financial Independence

Are you ready to revolutionize your fiscal plan and attain financial freedom?

In 2019, an AARP study found that 53% of adult households in the United States did not have an emergency savings account. The pandemic applied even more pressure to struggling Americans, exacerbating that anxiety. The fear of not having financial security can feel overwhelming, but you can take this moment to embrace the nation’s ethos of “land of the free and home of the brave” and apply it to your money management plan. Read on for five steps to follow to reach your personal money goals and achieve financial independence.

1. Expect the Unexpected with an Emergency Fund

It’s always been a smart idea to set aside some money in a savings account for the unexpected. The COVID-19 pandemic, and the economic and employment downturn it spurred, turned that theoretical possibility into a reality for many Americans. Having emergency cash in the bank can give you back the financial freedom that comes from having peace of mind. In the event of a global issue, the loss of your employment, or even an unexpected car repair or medical bill, an emergency fund is there to help. Though we’re all hopeful to soon put the pandemic and its effects fully behind us, one of the lasting lessons we can take away is that an emergency fund is a critical financial strategy.

Exactly how much you should set aside is a personal equation based on what you can afford today and your cost of living, but a good rule of thumb is to put away three to six months of expenses. You can sock it away in any savings account, but an FDIC- (or NCUA-) insured account at your bank or credit union is ideal. Set a monthly goal for how much you can contribute to savings and look for ways to automate the process.

Looking for a way to level up your emergency fund? Once you build it up to a certain amount, you may want to consider having your money work for you. If you exceed your emergency fund goals, keep saving and set aside some to invest in a low-risk fund to maximize yield.

Deciding to save into an emergency fund is a great way to regain control over your financial wellness and boost your overall well-being. Financial freedom can give you peace of mind that’s truly priceless.

2. Curb Spending and Increase Calm

Feeling financially free isn’t about being able to spend whatever you want today. It’s about knowing that you’ve saved enough that you don’t have to worry in the future. Setting a budget does force you to curb spending in the short term but setting up those fiscal guardrails is one of the surest paths to financial independence.

Having a realistic budget gives you a deep sense of calm and reassurance. Once you know how much money is coming in and how much you can spend, you have a holistic picture of where your money is going. Think of a budget as a road map. You wouldn’t set out on a cross-country trip without any idea of which road to follow. Living without a budget is like driving blind. Setting targets, defining priorities, and giving every dollar a job can help you get to where you need to go by putting you in the driver’s seat. What better way is there to achieve financial freedom?

Related Article: Financial Goal-Setting Tips to Help Achieve Your Money Goals

3. Make a Debt-Free Declaration

Being debt-free is one of the best markers of financial freedom. Getting out of debt and staying out permanently can help you save the money you need to have a stable future.

However, not all debt is created equal. There’s a difference between good debt and bad debt—the former can help you complete your education or buy a dream home, while the latter can bog you down with high-interest rates and unnecessary monthly payments. A 2020 Experian report showed that the average American owes approximately $92,727 in total debt—the highest amount ever recorded. If you’re in debt, you’re not alone. There are several strategies and steps that can help, but whichever path you take, make sure it’s both attainable and sustainable.

Before you buy something that will come with a high-payment plan, ask yourself if you a) need it and b) can actually afford it. Using an auto loan calculator or mortgage calculator can help you determine what fits into your budget.

4. Retirement Plan to Brighten Your Future

What is the ultimate financial freedom goal? For many people, it’s being able to have a secure, comfortable retirement in your later years. Here are a few simple things you can do today to help prepare for a great tomorrow:

- Maximize contributions to any tax-advantaged retirement savings accounts, like an IRA or a 401(k) plan

- Take advantage of any employer matching contributions so you can receive the full amount offered

- Diversify your investment portfolio with a mix of asset classes

It can be difficult to make short-term sacrifices in the name of a more comfortable future but keep your eye on the ball and remember you’re giving yourself the gift of financial independence.

5. Pay it Forward and Let Freedom Ring

If you’ve already accomplished all the items on this list and feel secure in your financial freedom, consider celebrating this July 4th holiday by helping others. Determine how much you can set aside for charitable giving and help support the missions and people who are important to you.

If you have younger loved ones, you can help set up or fund their 529 college savings account. It’s a great way to promote financial independence for the next generation, and maybe even help yourself along the way—some states let you claim a tax deduction for that kind of donation.

If you don’t have relatives that need help, consider donating to a child-focused charity, particularly one with a focus on education. Investing in the next era of earners can help us all enjoy more financial freedom in the years ahead.

Financial Independence on July 4th and Beyond

Freedom means many things for many different people, but on the fourth day of the seventh month of the year, we all come together to celebrate how lucky we are to be able to have the opportunities associated with independence. Financial security can help you feel more confident, in control, at peace, and, of course, free to live the life of your dreams.

Illuminated Advisors is the original creator of the content shared herein. I have been granted a license in perpetuity to publish this article on my website’s blog and share its contents on social media platforms. I have no right to distribute the articles, or any other content provided to me, or my Firm, by Illuminated Advisors in a printed or otherwise non-digital format. I am not permitted to use the content provided to me or my firm by Illuminated Advisors in videos, audio publications, or in books of any kind.

-

Seasonal Spending: Why we Overspend in the Summer

Curb Your Spending This Season with These Helpful Tips

Did you know that the summer season can affect your spending habits? Feeling the sun on your skin, the sand between your toes, and looking up at blue skies are all sure signs of the season, but you may notice a change in your bank account, too. It turns out more than half of all Americans—52%—tend to overspend in the summertime, according to a study from MassMutual. And another survey showed only 28% of respondents bothered to set a summer budget.

Why Does Summer Spending Affect Us?

What’s behind these free-for-all seasonal spending habits? Two-thirds of Americans say it’s a desire to “Make the most of the summer” that causes their spending to skyrocket. Of course, summer activities can cost more, too, and fear of missing out (also known as FOMO) may also contribute to slightly looser purse strings. Though this is likely the case in any year, it’s perhaps particularly so during the last years of the pandemic, when one of the only safe ways to gather has been when enjoying the great outdoors.

If you’d like to be more intentional about your summer spending habits, we can help. Use these tips to guide your spending habits so you can have a fantastic summer without breaking the bank.

Balance Fun and Responsibility

Staying inside all summer to avoid overspending isn’t a sustainable strategy. Of course, neither is spending money left and right on beach getaways and gourmet picnics. If you have children who are out of school in the summer, you’ll likely need a little cash on hand to keep them engaged and cared for.

Luckily, you can have your fun and save up, too—you just need to have a plan. Here’s a reasonable goal: pledge to spend a little bit more in the summer without going overboard. Here are some ways you can enjoy yourself without getting into financial trouble:

- Budget. Planning can help you stay on track during the summer. There are many different ways to budget, each with its own benefits and drawbacks. The important thing is finding something you can stick to, especially when summer temptations are plentiful. The best thing about budgeting is that when you know where your money is going, you give yourself permission to spend what you can. Need a new bathing suit? Want to schedule a long weekend away? If it fits within your financial goals, you can start packing your bag.

- Shop smarter. Many fun summer activities come with price tags. If you can get ahead of your seasonal spending, you can find innovative ways to save. Take outdoor furniture, beach necessities, and pool staples, for example—those are usually marked down as summer slides into fall. If you plan to stock up in advance, you can know you have what you need for a more affordable price.

- Start a summer fund. Throughout the year, you may find yourself saving in small ways. If you skip ordering takeout, stash those funds away. If you happen to make a little extra income one month, put it aside so you can enjoy it when the weather turns. Adding unexpected money to your fund is a great way to make sure you can maximize your summer fun, and it can be a motivating way to develop smarter spending habits, too.

- Focus on the long term. When the smell of barbecue is in the air and the waves beckon you from shore, it can be difficult to say no to overspending. But keeping your eyes on your long-term savings plan can help you keep your head when summer temperatures and temptations rise.

- Practice the pause. Picture this: you’re walking down the street in your favorite vacation spot and something in a store window catches your eye. What you want to do: go inside and buy it straight away. What you should do: keep walking and, if the urge to purchase it is still there a day or two later, check to see if it would fit in your budget. Pressing pause in that scenario can help save you from impulse buying, which rises in the summer months.

FOMO vs. Financial Goals

There’s so much to love about the summertime—the laid-back vibe, the beautiful weather, taking time off, and exploring new places. It’s natural to want to make the most of this time, but don’t let fear of missing out on summer fun dictate your financial wellbeing.

If you feel tempted to spend when you see the summer fun your friends and acquaintances are posting on social media, take a break from your social accounts for a while. If you need reminders to keep your eye on your long-term financial goals, write them out and post them on your fridge or keep them in a note on your phone.

Curbing seasonal spending habits can be tough but spending too much and suffering later can be an even bigger challenge. Keeping your wits about you during the warmer months can be a big benefit to you all year round.

Illuminated Advisors is the original creator of the content shared herein. I have been granted a license in perpetuity to publish this article on my website’s blog and share its contents on social media platforms. I have no right to distribute the articles, or any other content provided to me, or my Firm, by Illuminated Advisors in a printed or otherwise non-digital format. I am not permitted to use the content provided to me or my firm by Illuminated Advisors in videos, audio publications, or in books of any kind.

- Budget. Planning can help you stay on track during the summer. There are many different ways to budget, each with its own benefits and drawbacks. The important thing is finding something you can stick to, especially when summer temptations are plentiful. The best thing about budgeting is that when you know where your money is going, you give yourself permission to spend what you can. Need a new bathing suit? Want to schedule a long weekend away? If it fits within your financial goals, you can start packing your bag.

-

Strategies for Building Wealth in Your 50s

Now is The Time to Strengthen Your Finances and Finalize Your Retirement Plans

While it’s true that it’s better to begin saving earlier rather than later, it’s not too late to start building wealth in your 50s. In this decade of life, there are still smart moves you can make to help strengthen and grow your finances. Of course, as you get closer to retirement, the financial choices you make begin to carry more weight, so how you save and invest during this decade of your life will directly affect what your life looks like in retirement.

Below are six moves you can make in your 50s to build your wealth and better prepare yourself for retirement.

1. Build a Budget for Retirement

One of the most crucial aspects of proper money management in any decade of life is having a budget that appropriately reflects your financial reality and future goals. You’ll want to start by looking at how much you have saved for retirement, along with how your income and expenses are going to look as you get closer to that next phase of life. Don’t forget to factor in healthcare expenses as they’re one of the biggest roadblocks to financial security that retirees face. If your savings is still lacking, look at where you might be able to cut out some unnecessary spending in your life – now is really the time to singularly focus on saving as much as you can for the next stage of your life.

2. Eliminate Any Lingering Debt

While you’re still working and have a steady income that you can depend on, now is a good time to tackle your debts so that you can leave that financial stress behind once you retire. It’s financially savvy to start with your higher balances and any debts that have high interest rates. And while that’s a good idea, it may help you stay motivated to start with your smaller balances instead. Being able to watch yourself cross off debts one at a time can give you the motivation and confidence you need to finally face those larger balances. Whatever avenue you choose to take to stamp out your debts, what matters is that you stay committed to eliminating as much of them as possible before you leave the workforce.

3. Beef Up Your Retirement Accounts

With decades of work behind you, chances are you’ve been putting some money away into your retirement accounts consistently. Now that you’re in your 50s though, it’s time to maximize your contributions and get as much as you can out of compounding interest. So, start maxing out your 401(k), 403(b) and other retirement savings accounts. Once you hit age 50, you’re able to contribute an additional $1,000 into your IRAs, which can be a great super boost to your savings, too.

4. Rebalance Your Portfolio

As a young investor, taking more risks with your investments is smart, and it can be exciting, too. However, the closer you get to retirement the more you’re going to want to begin scaling back the risk in your portfolio. After all, you’re going to need to depend on that money to provide you with an income stream once you no longer have traditional paychecks. Take some time to review your portfolio and pull your money out of your riskier stocks to invest them into ones that are more stable. You’ll also want to be sure that your investments are properly diversified so that you don’t have all of your eggs in one proverbial basket.

Concluding Thoughts on Building Wealth in Your 50s

You can make smart retirement planning moves at any stage of life, but your 50s are the time to be sure that you have a firm grasp on your plans, and you know what steps to take before you finally say goodbye to your working life. If you’re not where you think you should be on your savings journey, that’s okay – you still have time make progress toward building wealth in your 50s. You just have to be diligent and intentional about it. The above tips are meant to help you boost your finances and bring you closer to accomplishing your money goals for retirement.

If you think you would benefit from a conversation about how to build your wealth in your fifties, or at any age for that matter, contact Lane Hipple Wealth Management Group at our Moorestown, NJ office by calling 856-638-1855, emailing info@lanehipple.com, or to schedule a complimentary discovery call, use this link to find a convenient time.

If you like what you’ve read, please share this article, and connect with us on your favorite social media channel.

Illuminated Advisors is the original creator of the content shared herein. I have been granted a license in perpetuity to publish this article on my website’s blog and share its contents of it on social media platforms. I have no right to distribute the articles, or any other content provided to me, or my Firm, by Illuminated Advisors in a printed or otherwise non-digital format. I am not permitted to use the content provided to me or my firm by Illuminated Advisors in videos, audio publications, or in books of any kind.