-

Lane Hipple Annual Gift Drive Delivers Once Again

From left: Thomas Lane, III (Partner, Lane Hipple), Melissa Rush (Director of Client Services, Lane Hipple), Maureen Ioannucci (School Counselor, South Valley Elementary), Heather Hackl (Principal, South Valley Elementary), Andy Hipple (Partner, Lane Hipple), and Mike Stringer (COO, Lane Hipple) Lane Hipple answers the (jingle) bell

Once again, the clients and staff of Lane Hipple put forth an overwhelming effort to help bring Christmas to local families who wouldn’t otherwise have the means to celebrate. For the third year in a row, we partnered with South Valley Elementary School, located in Moorestown, NJ.

Related article: Lane Hipple’s Annual Donation Drive (2023)

Upon receiving the families’ wish lists from Lane Hipple Director of Client Services, Melissa Rush, our clients took immediate action, delivering gift cards, toys, clothes, jackets, shoes, books, and more. The lists were curated by South Valley Elementary School Counselor, Maureen Ioannucci, who identified and worked together with the families who would benefit most from our annual gift drive.

“Words can not express the gratitude we have to you and your clients for their outpouring of generosity for our families. I wish I could take pictures of the families as they come to receive their gifts. There are tears, hugs and so much gratitude that their children will have a wonderful holiday!! Once again, thank you from the bottom of our hearts!”

– Maureen Ioannucci, SVE School Counselor

The total received from Lane Hipple clients included $4,800 in gift cards, $1,350 in cash donations used to purchase gifts, and all the items shown under the tree below.

To our clients:

We are immensely grateful for your incredible generosity! Our campaign to fulfill the holiday dreams of local families has surpassed all expectations. These children had an unforgettable holiday thanks to you! Their parents are overwhelmed with appreciation, making this experience truly feel like a Christmas miracle.

Wishing you a joyous holiday season and a prosperous new year.

-

Inheriting Wealth: How to Preserve and Grow Your Family’s Legacy

Inheriting wealth can be a life-changing event, but it also comes with a great responsibility to preserve and grow your family’s legacy. Whether you receive an inheritance from a parent, grandparent, or another family member, it’s important to have a plan in place to use the wealth wisely and continue to benefit future generations. In this article, we will provide guidance on how you might preserve and grow your family’s legacy after inheriting wealth.

Educate Yourself on Financial Management

To effectively manage an inheritance, it’s important to have a basic understanding of financial management. This includes knowledge of financial concepts such as budgeting, saving, investing, and debt management. If you don’t have this knowledge, consider taking a personal finance course or working with a financial advisor to develop a financial plan that aligns with your goals and values.

Assess Your Current Financial Situation

When inheriting wealth, it can be tempting to make big moves right away, such as paying off your mortgage. However, before making any decisions with your inherited wealth, take the time to assess your current financial situation. This includes reviewing your income, expenses, debts, and any existing investments or savings. By having a clear understanding of your financial position, you can make informed decisions about how to best use your inheritance to benefit your family now and into the future.

Consider Tax Implications

Inheriting wealth can also come with tax implications. Depending on the type and size of the inheritance, you may be subject to estate or inheritance taxes. It’s important to understand these tax implications and work with a financial advisor or tax professional to develop a tax strategy that minimizes your tax liability and preserves your family’s wealth.

Related Article: Passing an Inheritance To Your Children: 8 Important Considerations

Develop a Long-Term Plan

When inheriting wealth, you may want to develop a long-term plan that considers the needs of future generations. This includes setting financial goals, developing an investment strategy, and creating an estate plan. Research shows that up to 70% of families lose their wealth by the second generation, so having a long-term plan can help your family avoid that common fate.

Communicate with Your Family

Inheriting wealth can be a sensitive topic, and it’s important to communicate with your family about your plans and intentions. This includes discussing your long-term plan, setting expectations, and ensuring that everyone is on the same page. Open and honest communication can help prevent misunderstandings and ensure that your family’s legacy is preserved.

Consider Philanthropic Opportunities

Inheriting wealth can also provide opportunities to make a positive impact on your community and the world. Consider philanthropic opportunities that align with your family’s values and interests. This can include donating to charitable organizations, establishing a family foundation, or funding scholarships for deserving students.

Final Thoughts on Inheriting Wealth

Inheriting wealth can be a life-changing event, but it also tends to come with feelings of responsibility to preserve and grow your family’s legacy. To effectively manage an inheritance, it’s important to educate yourself on financial management, assess your current financial situation, consider tax implications, develop a long-term plan, communicate with your family, and consider philanthropic opportunities. By taking a thoughtful and strategic approach, you can preserve and grow your family’s wealth and leave a lasting legacy for future generations.

If you think you would benefit from a conversation about inheriting wealth, contact Lane Hipple Wealth Management Group at our Moorestown, NJ office by calling 856-638-1855, emailing info@lanehipple.com, or to schedule a complimentary discovery call, use this link to find a convenient time.

Illuminated Advisors is the original creator of the content shared herein. I have been granted a license in perpetuity to publish this article on my website’s blog and share its contents on social media platforms. I have no right to distribute the articles, or any other content provided to me, or my Firm, by Illuminated Advisors in a printed or otherwise non-digital format. I am not permitted to use the content provided to me or my firm by Illuminated Advisors in videos, audio publications, or in books of any kind.

-

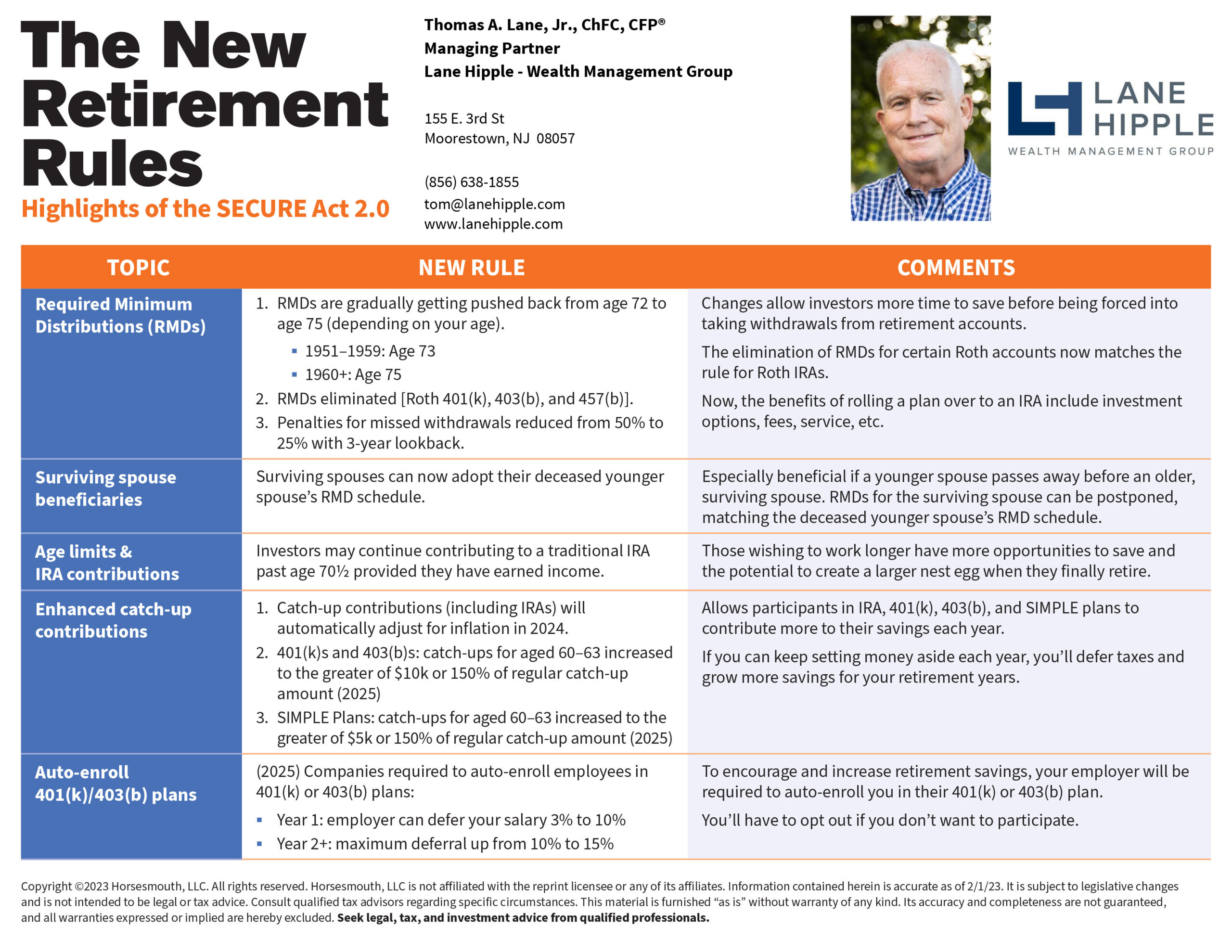

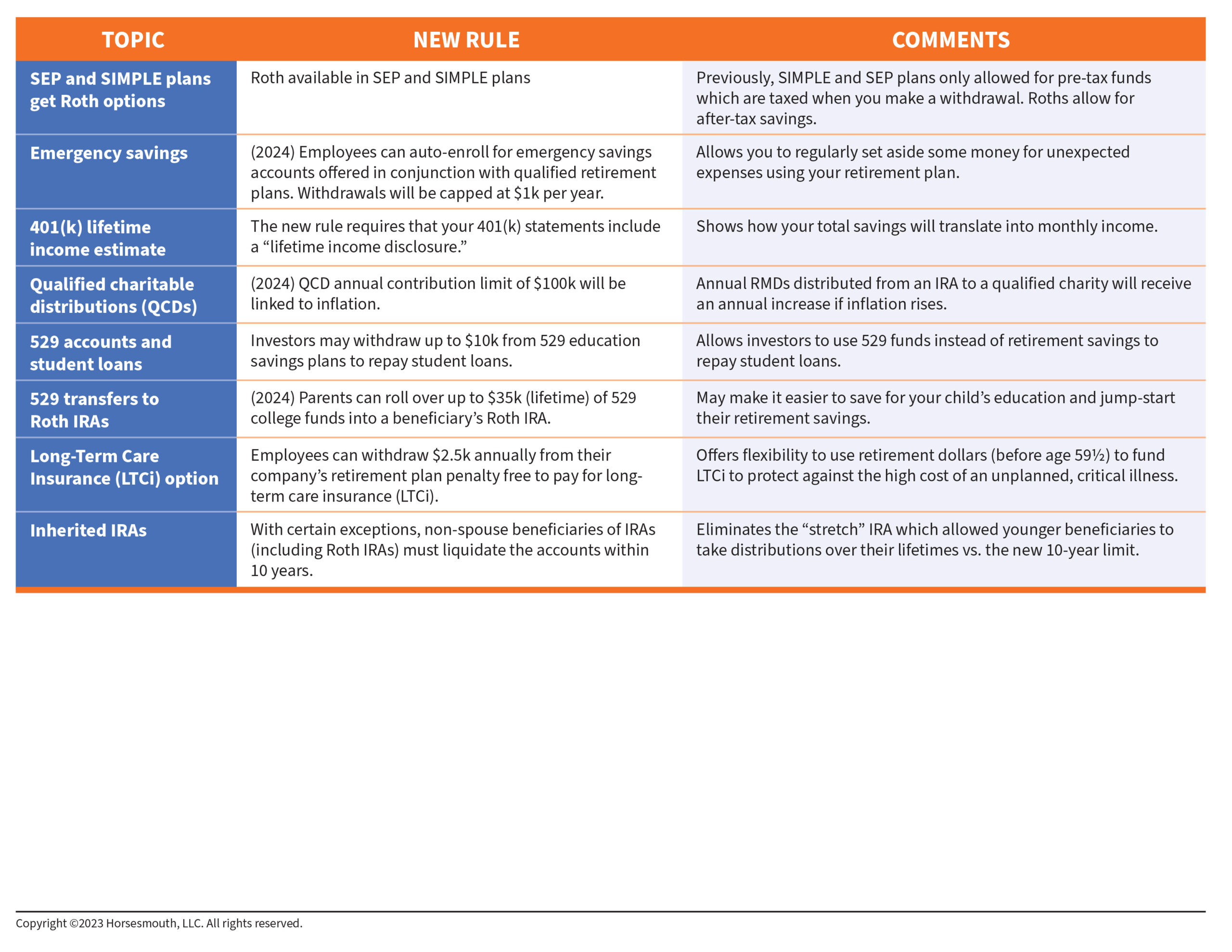

The New Retirement Rules

Highlights of the SECURE Act 2.0

-

5 Ways a Financial Advisor Can Help You Prepare for Tax Season

A Strong Tax Strategy is Part of a Thoughtful, Comprehensive Financial Plan

Tax season is upon us and, while not every financial advisor is a Certified Public Accountant (CPA), that doesn’t mean they can’t be helpful. Your financial advisor can assist you with making strategic tax moves throughout the year to help reduce your overall tax burden. As you read below, keep in mind that the sooner you begin having these conversations with your advisor about your tax strategy, the better off you’ll be at tax time.

Finding Ways to Maximize Your Tax Savings

There are many financial moves you can make throughout the year that will result in paying lower taxes, and a financial advisor will be educated about them. For example, some investment accounts let you make tax-deferred contributions, which can offer you the opportunity to save money on taxes while working to build your retirement savings. Take a company-sponsored 401(k), for instance. If you max out your contributions to this account, all of the money going in is pre-taxed, so you’ll be putting money away for retirement while reducing your tax bill in the present.

Keeping Record of Your Capital Gains and Losses

When filing your taxes, you’ll have to know how much you earned and lost from your investments for that year. A financial advisor will have an accurate and consistent record of your investments, which they can give to your accountant on your behalf. This will save you time and energy, and help you ensure you’re paying appropriate capital gains tax, without over-paying.

Developing a Tax-Savvy Gifting Strategy

There’s a lot to be gained when we gift our money to others. Not only do you get the intrinsic rewards associated with the joy and meaning that comes from helping others, but you can enjoy valuable tax benefits, too. Sit down with your financial advisor and discuss how you can gift your money in ways that ultimately help lower your tax bill, too. And this isn’t just for charities; if you want to give money to your family members for any reason, there are plenty of gifting strategies that let you transfer your wealth without a tax penalty. Check-in with your financial advisor before making any gifts so you can be sure to maximize the opportunity.

8 Considerations For Passing an Inheritance To Your Children

Minimizing the Tax Burden that RMDs Bring

Once you reach the age of 73, you’ll have to begin taking out Required Minimum Distributions (RMDs) from any IRA or 401(k) accounts that you have. While this comes as no surprise, often the uptick in your tax bill from having to pay income tax on those distributions does come as a surprise to retirees. A financial advisor will be able to provide you with management strategies so that you can lower your tax liabilities and be more prepared when the time comes to begin taking distributions.

Determining Tax-Efficient Investment Strategies

Although a financial advisor can’t necessarily protect you from capital gains tax, they will be able to help you by implementing strategies such as tax-loss harvesting, offsetting gains with losses, and avoiding issues such as “phantom tax,” which limit your overall tax liability. So, they’ll not only be able to help you manage and balance a portfolio, but they’ll be able to ensure you’re following the best investment strategies to benefit you the most when it comes time to file your taxes.

Do You Need a Financial Advisor to Assist with a Tax Strategy?

The world of taxes can be incredibly confusing, especially considering they’re constantly changing depending on the economy and new legislation. Having a financial advisor you trust is an important addition to your tax planning arsenal. A financial advisor can guide you throughout the year to ensure you’re making the best financial choices to help boost your tax strategy, with the ultimate goal of allowing you to save more of your hard-earned dollars.

If you think you would benefit from a conversation about your tax strategy, contact Lane Hipple Wealth Management Group at our Moorestown, NJ office by calling 856-638-1855, emailing info@lanehipple.com, or to schedule a complimentary discovery call, use this link to find a convenient time.

Illuminated Advisors is the original creator of the content shared herein. I have been granted a license in perpetuity to publish this article on my website’s blog and share its contents on social media platforms. I have no right to distribute the articles, or any other content provided to me, or my Firm, by Illuminated Advisors in a printed or otherwise non-digital format. I am not permitted to use the content provided to me or my firm by Illuminated Advisors in videos, audio publications, or in books of any kind.

-

5 investment ideas for small-business owners struggling to keep their finances liquid

Three local financial experts share their advice.

/cloudfront-us-east-1.images.arcpublishing.com/pmn/YJPKYC62CJFITAB5DO2ZNXQAWU.jpg)

Andrew Hipple has advice on how small business owners (and individuals) can take advantage of the rish in interest rates. (photo credit: Steven M. Falk / Inquirer Staff Photographer) Written by Gene Marks

Even as commercial lending rates have more than doubled in the last year, interest rates earned on checking, money market and savings accounts remain stubbornly low as banks seek to maintain their profitability.

That’s not helpful for business owners, who need to earn money on their cash reserves while keeping enough liquidity to meet faily working capital needs. Options remain limited, but the environment is slowly changing, and a number of investment choices with minimal risks are emerging.

Click here to read full article from the Philadelphia Inquirer, featuring Andrew Hipple CFP®, Partner at Lane Hipple Wealth Management Group.