-

College Student Financial Tips for the Young People in Your Life

How to Help a New College Student Prepare for Success

The first semester of college is an exciting time, and the perfect moment to pass along financial tips for your new college student. Oftentimes, it’s the first chance young people have to leave the nest, spread their wings, and experience the ups and downs that come with financial freedom.

Your kids have come a long way from the days of the tooth fairy and piggy banks as fiscal cornerstones. It’s critical that young people enter into this next stage of life with everything they need to not only succeed academically, but financially, too. The college student financial tips below are helpful topics to discuss with the new college students in your life to help them start off on the right foot.

Tip #1: Learn Budgeting Basics

There are many different ways to budget and prioritize. You can give your child a big advantage by sitting down and coming up with a reasonable and realistic financial plan for fixed items, extracurriculars, academic needs, and even an emergency fund to prepare for the unexpected.

Then determine the best way to keep track of the budget. There are several apps loaded with features that can make it easy to stay on track. Or, if your college student is a fan of spreadsheets, they can put their math skills to good use with some easy formulas and templates. Better yet, see if they can sign up for a budgeting, financial skills, or economics course that can help integrate their personal and academic goals.

Tip #2: Be Wary of Borrowing

Student loans are a staple of college education financing for many students these days. But even though they’re available, it pays to be wary of how much you borrow and how you use the funds. Though there are plenty of temptations in campus life—spring break, shopping, or late-night pizzas—student loan dollars should only be used for tuition, books, and necessary living expenses.

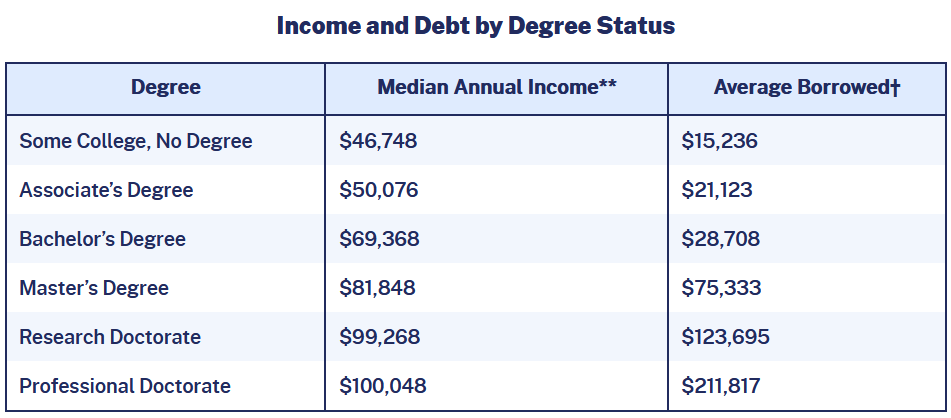

Depending on how savvy your child is with financial situations, you may want to suggest that you help take them through the loan paperwork before they sign it. Student loan debt in the United States totals a whopping $1.75 trillion dollars, and the average U.S. household with student debt owes $62,913. So, it’s important to be clear that there’s a lot on the line.

SOURCE: www.educationdata.org *Among workers aged 25 years and over; based on average weekly earnings of full-time wage and salary workers.

†Cumulative student loans only (no Parent PLUS); data collected between 2015 and 2018, currency inflated to 2021Q2 values to match income data collection period; amount borrowed is not equivalent to current debt.Tip #3: Prioritize Education

We want our kids to make the most of college on the academic front, but we also hope that it’s a fun and enjoyable time in their lives. It’s a new and exciting environment, and often the first chapter of their lives in which they are able to branch out on their own and discover who they are and what they want out of life. Of course, life is about balance, and new students need to walk the line between the call of adventure and important academic obligations. Falling behind can quickly lead to failing a class. Not only will that hurt their academic standing, but if they have to make up the class, they’ll likely have to pay for it again.

Tip #4: Credit Is Complicated

Credit cards can seem a bit like an “easy button” for young people tempted by the latest fashions, technology, and experiences. Fortunately, by law, credit card companies aren’t permitted to market on college campuses or issue cards to anyone under 21 without proof of income or an adult cosigner.

You can, of course, add your child to your card as an authorized user, but be sure to limit use to emergencies only and discuss the dangers of high-interest debt.

Tip #5: Live by the Textbook

Textbooks are notoriously expensive—over the course of a college career a student can easily exceed thousands of dollars on textbooks alone. Buying used books can save some funds, as can sharing costs with a study partner who is in the same class. Renting is also an option—there are plenty of companies online that will let you rent or borrow books one semester at a time for a much lower price point. Make certain your student knows that buying new isn’t the only option.

Tip #6: Master the Basics

Your child may be book smart, but often the biggest life lessons aren’t covered in school. Make sure your new college student has a good grasp of basic living skills. Teach them how to cook on a budget instead of ordering food out. That one habit alone can save them thousands of dollars. Encourage them to carpool or take public transportation instead of relying on cabs or Uber. Making sure they do their own laundry can also ensure their clothes last for years instead of months. These may sound like basic life skills instead of college student financial tips but, when combined, they can help your child prepare for a successful college career and a financially responsible life ahead.

College Sets the Course

Your child’s college years are consequential on several fronts. How your new college student does in their academic career can have a big impact on their career prospects, of course, but there’s more to it. Looking beyond grades, it’s also a time during which they discover who they are and what they’re made of. Giving sound advice can help them feel confident and accomplished and set them up for a future they (and you) can be proud of. So, use these financial tips for your new college student to help them chart a successful course through college and beyond.

If you think you would benefit from a conversation about personal finance or broader financial planning topics, contact Lane Hipple Wealth Management Group at our Moorestown, NJ office by calling 856-638-1855, emailing info@lanehipple.com, or to schedule a complimentary discovery call, use this link to find a convenient time.

Illuminated Advisors is the original creator of the content shared herein. We have been granted a license in perpetuity to publish this article on our website’s blog and share its contents on social media platforms. We have no right to distribute the articles, or any other content provided to our Firm, by Illuminated Advisors in a printed or otherwise non-digital format. We are not permitted to use the content provided to us or my firm by Illuminated Advisors in videos, audio publications, or in books of any kind.